The title “IDC Report: Garmin Wins, Apple Loses Big, Everyone Else loses” sums up IDC’s take on their own research. You can read their press release but I’ve included it below as it gives a nice table and a link to a nice chart.

It’s nice to see that Garmin’s CHRONOS is already contributing significantly to these shipments ?!? Ok, IDC are ‘measuring’ TRADE/B2B type shipments, presumably, rather than a couple of weeks of retail sales of that item (!) so it’s quite possible that Garmin have been shipping tens of thousands of CHRONOS devices to the various retailers – I doubt it. But possible. It’s more likely that Garmin are performing better with volume sales at the lower end of the market where, almost by definition, there will be more units shipping.

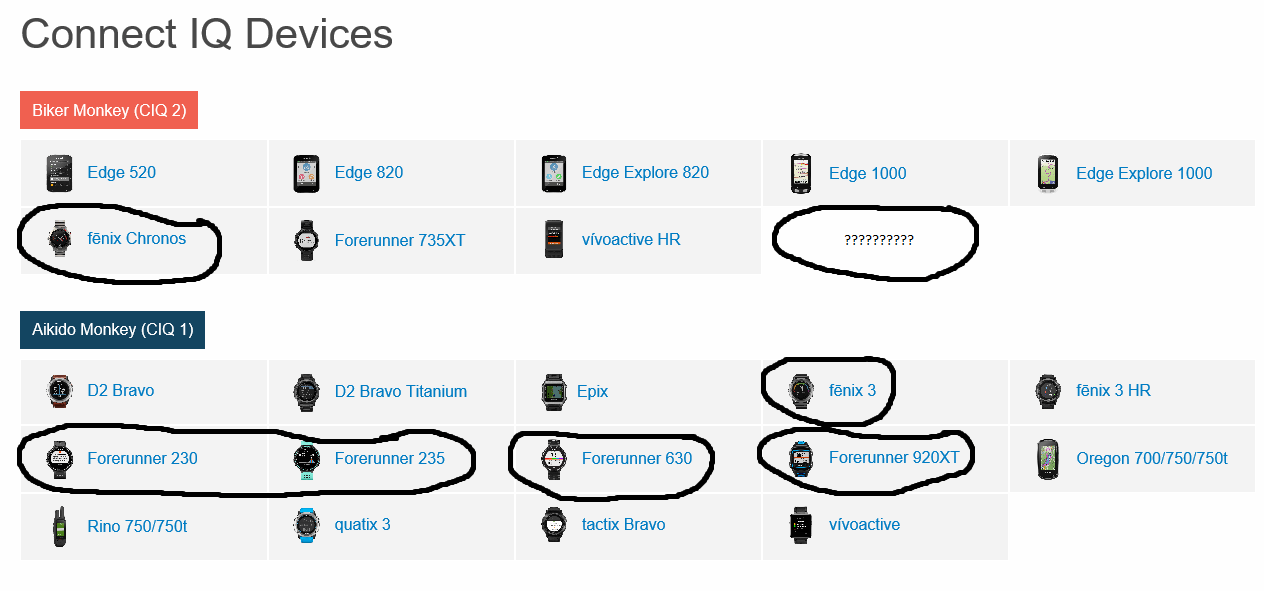

The IDC report also sys that “Data only includes smartwatches capable of running third party applications on the device itself”. OK, fair enough. Let’s take that at face value. So that means we are only looking at the following Garmin devices right?

So let’s delve further. We’ve already established that they are talking about trade sales. So trade sales will probably favour newer lines like the Edge 820 so that the retailers can stock up for Xmas. Fair enough. Oh, but wait a minute I don’t recall ever seeing anyone wear an Edge 820 on their wrist, the report is about smartwatches right? Not super-smart cycling computers!?!

From the above image, the only Garmin CIQ smartWATCHES likely to be shipping in any bulk are the 235, 230, 630 (?), 920 (?), 735(?), vivoactive/HR, and fenix 3/3HR – and many of those are end-of-line and approaching replacement ie ALL the ones listed in the image as CIQ 1 are approaching end-of-line status. I can quite believe the Vivoactive HR is shipping lots (I’ve heard it’s doing well), the 735 I’ve heard is not doing so well and the Chronos just can’t be making much impact on the figures surely at $1000-$1500?

So now I’m confused. Again! yes, I know!

600,000 of those globally? I’ve no idea to be honest, I suppose it’s possible. But I suspect that IDS might be including all CIQ devices….which are not watches OR they are including non-CIQ watches which are not SMART. And I suspect that some commentators (not analysts) are including expensive CHRONOS units as a causative factor just because that was in Garmin’s last press release!!

Anyway, I’m sure Mr Garmin will take that as a win either way and I am sure Garmin ARE doing well. Good for them.

I probably somewhat agree with IDC’s comments on Apple. Agree in the sense that the period in question is probably a statistical/seasonal anomaly going from peak sales/shipment of v1 to v2 just starting out in the market. So when IDC speak of a rebound then their figures may well show that for the next quarter.

I’m not quite sure what’s going on with AndroidWear2 but my understanding is that this has slipped on delivery to 2017 so, quite plausibly, that will have caused some vendors wanting to use that platform a headache in the run up to Christmas – ie they can’t release some new devices relying on that platform.

dcrainmaker also quite rightly tweets about the omission of 1 million Fitbit Blaze devices.

Still what’s a million units when it comes to accurate trade sales figures?!

Looking for more general causative factors:

It’s also interesting to hear Senior Researcher, J Ubrani’s comments, below, “Having a clear purpose and use case is paramount“. Yes there is clearly some truth in that.

- BUT the angle for his analysis should really be about CUSTOMER NEEDS/WANTS and not about new technology per se. Yes there is an argument that technology can CREATE new wants/needs but I think what we are seeing with wrist-based smartness is that people are not really seeing how technology bought for them as a present or corporate necessity can always help them – SPORTS/FITNESS is an obvious exception and one which most vendors are edging towards in some form; and

- What if somebody invented a better mouse trap? would people buy it if the existing ones work perfectly well? Why upgrade your Fitbit to a smart(er) one that looks similar?; and

- What if somebody had a first generation activity tracker (non smart) might they not be put off by the general concept and doubt the usefulness of a smarter version?

Anyway, Garmin are clearly doing well.

Rant over. Back to the day job

——————————————————————————————————————————————————————————————

Smartwatch Market Declines 51.6% in the Third Quarter as Platforms and Vendors Realign, IDC Finds

24 Oct 2016

FRAMINGHAM, Mass., October 24, 2016 – The worldwide smartwatch market experienced a round of growing pains in the third quarter of 2016 (3Q16), resulting in a year-over-year decline in shipment volumes. According to data from the International Data Corporation, (IDC) Worldwide Quarterly Wearable Device Tracker, total smartwatch volumes reached 2.7 million units shipped in 3Q16, a decrease of 51.6% from the 5.6 million units shipped in 3Q15. Although the decline is significant, it is worth noting that 3Q15 was the first time Apple’s Watch had widespread retail availablity after a limited online launch. Meanwhile, the second generation Apple Watch was only available in the last two weeks of 3Q16.

“The sharp decline in smartwatch shipment volumes reflects the way platforms and vendors are realigning,” noted Ramon Llamas, research manager for IDC’s Wearables team. “Apple revealed a new look and feel to watchOS that did not arrive until the launch of the second generation watch at the end of September. Google’s decision to hold back Android Wear 2.0 has repercussions for its OEM partners as to whether to launch devices before or after the holidays. Samsung’s Gear S3, announced at IFA in September, has yet to be released. Collectively, this left vendors relying on older, aging devices to satisfy customers.”

“It has also become evident that at present smartwatches are not for everyone,” said Jitesh Ubrani senior research analyst for IDC Mobile Device Trackers. “Having a clear purpose and use case is paramount, hence many vendors are focusing on fitness due to its simplicity. However, moving forward, differentiating the experience of a smartwatch from the smartphone will be key and we’re starting to see early signs of this as cellular integration is rising and as the commercial audience begins to pilot these devices.”

Top Five Smartwatch Vendors

Apple maintained its position as the overall leader of the worldwide smartwatch market, yet it posted the second largest year-over-year decline among the leading vendors. Its first-generation Watches accounted for the majority of volumes during the quarter, leading to the significant downturn for the quarter. Its Series One and Series Two did little to stem that decline, although with lower price points and improved experiences, Apple could be heading for a sequential rebound in 4Q16.

Garmin posted the largest year-over-year increase among the leading vendors, thanks to its growing list of ConnectIQ-enabled smartwatches and the addition of the fenix Chronos. Whereas other smartwatches attempt to be multi-purpose devices, Garmin’s smartwatches focus on health and fitness, and the applications reflect that strategy. Its total volumes helped close the gap further against a declining Apple and extended its lead ahead over Samsung.

Samsung finished 3Q16 slightly higher from a year ago on the strength of its aging Gear S2 smartwatches. These still remain one of the few smartwatches on the market that feature full-time cellular connectivity. The company introduced its follow-up, the Gear S3, with a Bluetooth-only version as well as a cellular version, but it has yet to be released to the market.

Lenovo (Motorola) suffered the largest year-over-year decline among the leading vendors, with multiple channels selling out of Moto 360 devices (both first and second generation) and a scarcity of its recently released Moto 360 Sport smartwatch. In addition, 3Q16 marks the first time in which Motorola did not introduce a new smartwatch in time for the holiday quarter, adding to its decline in the market.

Pebble arguably kicked off the smartwatch category with its original Kickstarter campaign in 2012. Since then the company has launched multiple variants of the Pebble watch and also introduced a new timeline-based user interface, though none of them achieved mass success. After another successful Kickstarter campaign in early 2016, Pebble released the Pebble 2 (oddly enough, the third generation) late in the third quarter. The new Pebble 2 is the first watch by the company to include a heart-rate sensor and has an overall focus on fitness.

| Top Five Smartwatch Vendors, Shipments, Market Share and Year-Over-Year Growth, 3Q 2016 (Units in Millions) | |||||

| Vendor | 3Q16 Unit Shipments | 3Q16 Market Share | 3Q15 Unit Shipments | 3Q15 Market Share | Year-Over-Year Growth |

| 1. Apple | 1.1 | 41.3% | 3.9 | 70.2% | -71.6% |

| 2. Garmin | 0.6 | 20.5% | 0.1 | 2.3% | 324.2% |

| 3. Samsung | 0.4 | 14.4% | 0.4 | 6.4% | 9.0% |

| 4. Lenovo | 0.1 | 3.4% | 0.3 | 6.2% | -73.3% |

| 5. Pebble | 0.1 | 3.2% | 0.2 | 3.3% | -54.1% |

| Others | 0.5 | 17.2% | 0.6 | 11.5% | -27.2% |

| Total | 2.7 | 100.0% | 5.6 | 100.0% | -51.6% |

| Source: IDC Worldwide Quarterly Wearable Device Tracker, October 24, 2016 | |||||

Table Notes:

- Data is subject to change.

- Vendor shipments are branded device shipments and exclude OEM sales for all vendors.

- Data only includes smartwatches capable of running third party applications on the device itself. Examples include Apple Watch, Moto 360, Gear S2. Devices like the Fitbit Blaze and Withings Activité are excluded since IDC considers these as “Basic Wearables” that do not run third party applications.

- All other wearable form factors (i.e. earwear, clothing, wrist bands, etc.) are excluded.

https://web.archive.org/web/20181125040003/https://accounts.icharts.net/icharts/embed/MH/WwypE

This chart is intended for public use in online news articles and social media. Instructions on how to embed this graphic are available by selecting here.

About IDC Trackers

IDC Tracker products provide accurate and timely market size, vendor share, and forecasts for hundreds of technology markets from more than 100 countries around the globe. Using proprietary tools and research processes, IDC’s Trackers are updated on a semiannual, quarterly, and monthly basis. Tracker results are delivered to clients in user-friendly excel deliverables and on-line query tools. The IDC Tracker Charts app allows users to view data charts from the most recent IDC Tracker products on their iPhone and iPad. The IDC Tracker Chart app is also available for Android Phones and Android Tablets.

IDC’s Worldwide Quarterly Mobile Phone Tracker, please contact Kathy Nagamine at 650-350-6423 or kn*******@*dc.com.

About IDC

International Data Corporation (IDC) is the premier global provider of market intelligence, advisory services, and events for the information technology, telecommunications, and consumer technology markets. With more than 1,100 analysts worldwide, IDC offers global, regional, and local expertise on technology and industry opportunities and trends in over 110 countries. IDC’s analysis and insight helps IT professionals, business executives, and the investment community to make fact-based technology decisions and to achieve their key business objectives. Founded in 1964, IDC is a wholly-owned subsidiary of International Data Group (IDG), the world’s leading media, data and marketing services company. To learn more about IDC, please visit www.idc.com. Follow IDC on Twitter at @IDC.

Last Updated on 16 January 2026 by the5krunner

My favourite kit and nutrition

- Injinji – Runners protect your toes. Avoid discomfort and minor injury. Run more. Run faster. I use them.

- Garmin 90-degree charging adapter — The small adapter that keeps your charging cables tidy. Essential for race day. I use one.

- Garmin charging puck — the fastest and most reliable way to top up your Garmin before a session. I use one.

- Ravemen FR300 — Front light that mounts directly under your Garmin or Wahoo head unit. Keeps your bars clean and your beam pointed where it matters. I use one.

- Body Glide – The blue anti-chafe stick that all swimmers and many runners use. I use it.

- Maurten — The race nutrition trusted by elite athletes. Gels and drink mixes engineered to be easy on the stomach. I use them.

- Garmin Varia RTL515 — A radar rear light that alerts you to vehicles approaching from behind. Pairs with your Edge or Garmin watch. I use this model.

- Favero Assioma Pro RS2 — The power-meter pedals most serious cyclists choose. Accurate, easy to move between bikes. I use this model.

- Garmin Forerunner 970 — A serious choice for a pro-grade triathlon watch. I use this.

- Polar H10 — My daily driver for accurate, waking HRV readings.

- Wahoo ELEMNT Roam 3 — The bike computer that has the feature Garmin lacks: usability. I use mine on most rides.

Reader-Powered Content

This content is not sponsored. It’s mostly me behind the labour of love, which is this site, and I appreciate everyone who supports it.

Support the site: Follow (free, fewer ads) · Subscribe (paid, ad-free) · Buy Me A Coffee ❤️

All articles are written by real people, fact-checked, and verified for originality. See the Editorial Policy. FTC: Affiliate Disclosure — some links pay commission. As an Amazon Associate, I earn from qualifying purchases.

tfk is the founder and author of the5krunner, an independent endurance sports technology publication. With 20 years of hands-on testing of GPS watches and wearables, and competing in triathlons at an international age-group level, tfk provides in-depth expert analysis of fitness technology for serious athletes and endurance sport competitors. ID

This only really proves the old adage of being able to prove whatever you want with statistics. Garmin showed a good percentage growth but that’s easy to do if your previous sales are tiny (which they were). Apple launched their watch and didn’t update it for 18 months so of course sales slowed. Garmin by contrast launch something new almost weekly it seems. IDC are just trying to keep their name front and centre and everyone knows that no matter how tenuously you go about it, “Apple is doomed” always generates web traffic.

What is interesting is how IDC can create links where none exist in the real world. If you were to ask the Garmin customers why they wanted a smart watch you would get a lot of blank stares, they wanted a fitness/GPS watch This would probably run counter to the wishes of Garmin as they want to compete with Apple in this segment. However it will take a massive mind share change for customers to start looking at Gamin as smart watches rather than GPS devices. Apple have the advantage of having a “watch” that as it develops can take on other duties.

I suppose it is all semantics and just reinforces that information should not just be taken at face value.

“they wanted a fitness/GPS watch ” – yep I don’t think anyone would go into a shop and say “can I have a smartwatch” they would want a watch that does X, Y and Z.

What’s actually funny, is that in doing some digging, I think by IDC’s rulebook it was actually Suunto that had the first smartwatch (in market) that allowed 3rd party apps, with the Ambit1 in Nov 2012. I’m not aware of anything sooner.

Go figure that now, full circle, they’ve left that stage in terms of apps.

The irony of the Spartan not being smart hadn’t escaped me either!