Garmin 2022 – Full year sales crash for Fitness. Company maintains margins, Cash Flow Crashes by 22%

Garmin’s full results for 2022 are out.

They show a gradual decline overall for the company BUT with increased margins. That should be good news for many Garmin employees who are worried about job security.

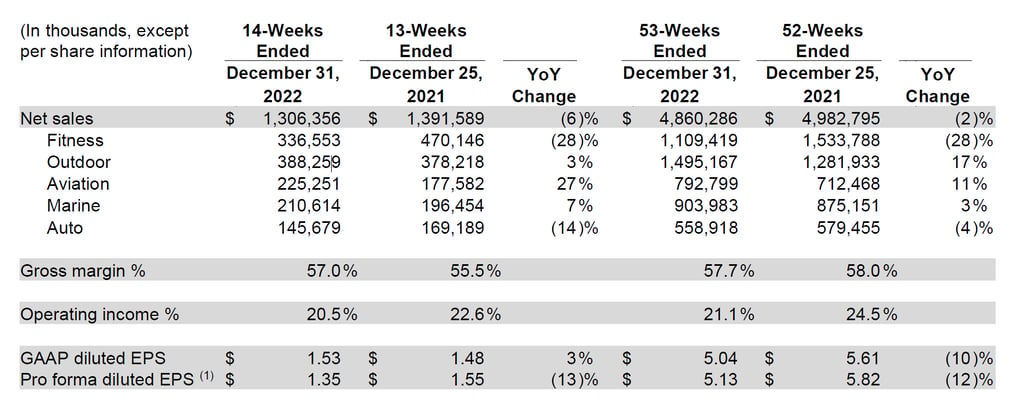

However, a significant concern is the sales crash of the fitness segment of the business, which includes cycling and Forerunner but excludes Fenix. The fitness segment fell by 28% both for the full year and for Q4. This level of decline may be heavily skewed by cycling products, which have also been experiencing similar levels of decline across the competition.

The sales in the OUTDOOR segment seem to be holding up, with annual growth remaining healthy, but Q4 growth of 3% demonstrates an obvious slowdown. However, the notes to the financial statement indicate that the growth in the OUTDOOR segment is coming from HANDHELDS, and not from Fenix/Epix sales.

Putting this all together, it appears that 2023 is not going to be an easy year for Garmin sports products ie watches and bike products.

Here’s what Garmin said

Fitness:

Revenue from the fitness segment decreased 28% in the fourth quarter, with declines across all categories. Gross and operating margins were !!49% and 12%!!, respectively, resulting in $40 million of operating income. During the quarter, we launched Bounce, our first LTE-connected kids smartwatch. Bounce offers two-way text and voice messaging, as well as real-time location tracking. Bounce also offers kids fitness tracking, games, and allows parents to assign chores and give rewards.

Outdoor:

Revenue from the outdoor segment grew 3% in the fourth quarter primarily due to growth in handhelds and services. (ie NOT FENIX and NOTE EPIX) Gross and operating margins were 64% and 34%, respectively, resulting in $132 million of operating income. During the quarter, we launched the second-generation MARQ luxury smartwatch collection built with Grade-5 titanium, sapphire glass, and a vibrant AMOLED touchscreen display. [Garmin]

Note: the 49% margin for the FITNESS segment is BAD news. Garmin aims to keep margins above 50% so any parts of the business dragging the average down are a cause for concern.

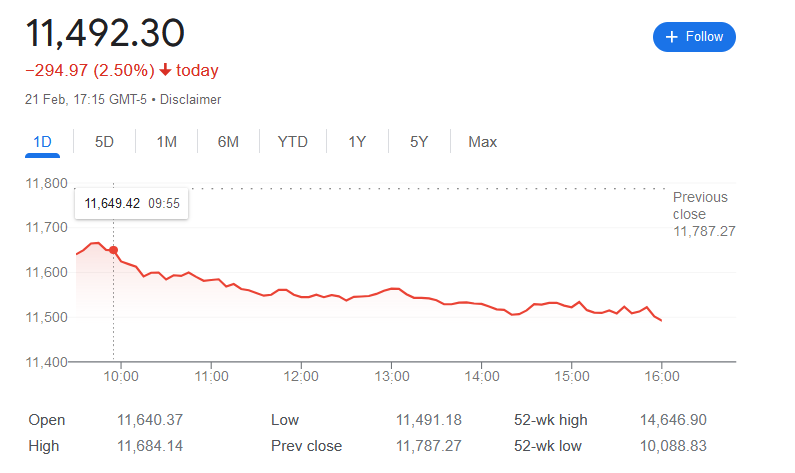

The markets have NOT reacted badly to this news. Clearly, they expected something similar. Over the last 5 days, Garmin has only very slightly underperformed falls on the tech-heavy NASDAQ (GRMN is listed on NYSE as of 2021).

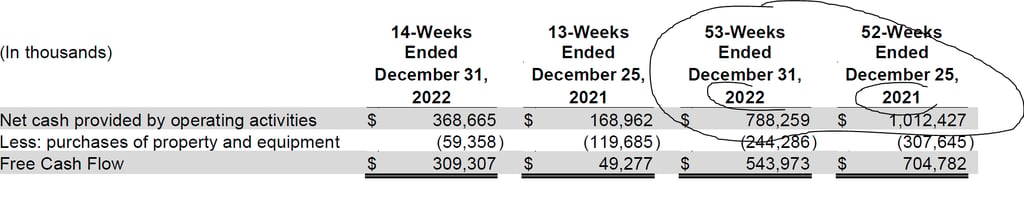

Corporate Cash Position

This chart from Garmin clearly shows that the cash it generates from normal activities has fallen by 22% from $1000m to $788m

Presumably, the Q4 cash situation compared to 2021 was improved by reducing expenditure on property/equipment

Will new products turn this around?

New products and new customers are the only way Garmin is going to turn this around in the short term and as I posted earlier today, don’t expect too much from new products by Garmin in 2023 – last year was the bumper year for new products. Sure we might get an Epix 2X and Epix 2S but neither of those will impact the FITNESS segment. FITNESS will only benefit from the new Forerunner 965, 265/265s and Edge 840/840 Solar/540 over the next few months and maybe a couple of new Venu models later in the year. Sales for all of these will be ‘alright’ but don’t expect sparks to fly in the current climate.

Garmin – What next (later in 2023, after the 965 and Edge 540)

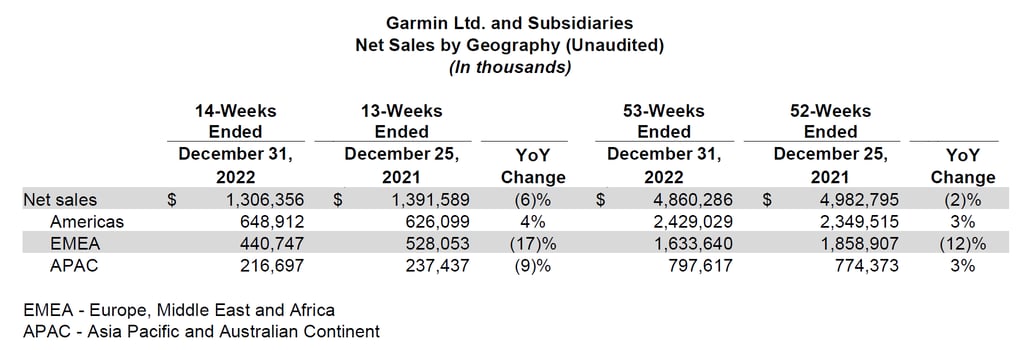

The view that product innovation must turn this around is supported by the sales figures that paint a bleak economic picture in some regions. Europe is ‘stuffed’, it’s effectively in recession and declining with a poor outlook. Markets do not seem to fully appreciate that the Ukraine War has forever changed the cheap energy supplies that underpin German/Italian/European heavy industry ie the EU’s cheque book is ripped up.

Asian economies, in total, are probably also now declining for Garmin and in any case, the growth that is reported elsewhere in the region by other media outlets, for example in India, is at the bottom end of the price spectrum which is definitely not Garmin’s forte.

However, as we see here, the Americas are still growing (yay!). That growth might taper off slightly in the course of 2023 but I would still have a positive outlook for opportunities there for the company and for the region once on-shoring gathers pace. The USA obviously also has energy independence which is fundamentally important for underpinning its economic growth going forward.

Also Note

These points are noteworth but to a lesser degree so I just add them here as one line notes.

Looking ahead, Garmin is internally combining two segments, AUTO and OUTDOOR. It’s possible that there were some layoffs resulting from this decision, or perhaps some employees were relocated to other parts of the organization.

In January 2023, the Company combined the consumer auto operating segment with the outdoor operating segment. [Garmin]

R&D spend grows but this only means that the engineers got a pay rise.

Research and development increased 5% primarily due to engineering personnel costs [Garmin]

2023 will be static in terms of overall revenue

Revenue $5.00Bn [Garmin]

2022 had positive cashflow

Fourth quarter of 2022, we generated approximately $309 million of free cash flow [Garmin]

In 2023 Garmin intend to maintain the dividend payment and to further increase shareholder value by completing the remaining half of its share buyback program

approximately $93 million remaining as of December 31, 2022 in the share repurchase program which is authorized through December 29, 2023. [Garmin]

Take out

Here is what I said last quarter and I don’t expect the outlook to materially change.

Strategic Opportunity: I think Garmin may soon realise that they have entered several procuct-related cul de sacs, albeit large and profitable ones. The only major new strategic opportunities I see for Garmin are geographical and those linked to AMOLED. I’m not so sure that Solar and Satellite-based personal safety capabilities will become that important for Garmin in the longer term.

I’ll double down on that and go one step further.

AMOLED is a major opportunity for Garmin however it’s only nice to have. There will simply be many people out there who cannot afford this or who might delay an upgrade for a year or two more than they otherwise might. Furthermore, in contracting markets, the supply of new, unsullied customers looking for their first watch or bike computer is also getting tighter.

Thus AMOLED sales WILL come for Garmin… just not as many as it would like.

On the one hand, you need to consider Garmin’s competition and keep in mind that Garmin is in a stronger financial position than many of its competitors, with $1.3 billion in cash equivalents on hand. This is a significant advantage for Garmin. However, it’s worth noting that its cash flow position is also deteriorating, and the positive cash flow generated by the business for the full year decreased by around 20% compared to the previous year. While this may not sound ideal, it’s important to recognize that when compared to some of its competitors, Garmin is still generating cash rather than burning it.

It’s also worth revisiting the geopolitical outlook. Many US tech companies have already begun to bring their operations back to North America. Garmin has historical ties to Taiwan, where there will soon be elections and where the pro-independence party currently polls well. There is a significant risk of disruptive Chinese action against that country in the next 5 years, the risk includes war.

I do NOT have a position in Garmin or related companies and I’d rather not have one right now!

Source: Garmin,

Last Updated on 27 January 2026 by the5krunner

My favourite kit and nutrition

- Maurten — the race nutrition trusted by elite athletes. Gels and drink mix engineered to be easy on the stomach.

- Garmin 90-degree charging adapter — the small adapter that keeps your charging cable tidy at the stem. Essential for race day.

- Garmin charging puck — the fastest and most reliable way to top up your Garmin before a session.

- Ravemen FR300 — front light that mounts directly under your Garmin or Wahoo head unit. Keeps your bars clean and your beam pointed where it matters.

- Garmin Varia RTL515 — radar rear light that alerts you to vehicles approaching from behind. Pairs with your Edge or Garmin watch.

- Stryd — the footpod that brings running power to your Garmin. The single most useful running upgrade I have made.

- Favero Assioma Pro RS2 — the power meter pedals most serious cyclists end up choosing. Accurate, easy to move between bikes.

Reader-Powered Content

This content is not sponsored. It’s mostly me behind the labour of love, which is this site, and I appreciate everyone who supports it.

Support the site: Follow (free, fewer ads) · Subscribe (paid, ad-free) · Buy Me A Coffee ❤️

All articles are written by real people, fact-checked, and verified for originality. See the Editorial Policy. FTC: Affiliate Disclosure — some links pay commission. As an Amazon Associate, I earn from qualifying purchases.

tfk is the founder and author of the5krunner, an independent endurance sports technology publication. With 20 years of hands-on testing of GPS watches and wearables, and competing in triathlons at an international age-group level, tfk provides in-depth expert analysis of fitness technology for serious athletes and endurance sport competitors. ID

The days of the huge “Apple watch also made non-Apple people consider expensive wrist computers” change seem to be over an now it’s a stable market, not a fast growing one?

Note that the Garmin pdf says consumer auto merged with *outdoor*, not with fitness, even if your version sounds a bit more plausible. Perhaps it’s an intermediate stage of splitting up outdoor by moving those rugged handhelds and the like to automotive and wearables to fitness? That would kind of make sense I think

$1.3b a quarter is a good business, just not Apple-good. ~$725m is from the fitness and outdoor categories. On the other hand Apple wearables and accessories is $13.5m for the quarter which was -8%. -2% is actually pretty good for this environment. It’s -12% for Europe and +2% and +3% for America and Asia respectively. The Europe decline may be driven by exchange rate issues and the Ukraine war.

I don’t really understand why they have an outdoor and a fitness operating division. They seem to overlap a lot in the target market. The devices are so similar but they independently develop features and merge them across product lines.

They absorbed consumer auto into the outdoor division, but the fitness division remains independent.

Is there not a problem with their move to yearly release cycles (965, 955) is that it takes Garmin over a year to have functional stable firmware after they release products?

😉

the 965/265 are not really a new model rather an AMOLED variant of an existing one. at least that’s how i think of it

Also the insight 2 is technically in their outdoor segment, but is a very cheap fenix/955 in terms of software. These segments are a mess…..

Garmin could fix this all if they got a little more intelligent about how they do updates.

They should market a watch with a service. “say, 1 year of free updates with each watch”

Then charge a nominal fee for new features, not but fixes, new features. Say you have a 265 and you want and you wanted to add chronic load (assuming they didn’t give it away for free), garmin could add it for say 5$ or something. They could also market more years of updates, say 25$ per year for all new features.

I think this would fix a lot of their problems with people complaining about buying a new watch and not getting updates, plus it would add a small yet stable income stream with a frequency. Unless they got crazy with software upgrade costs, this could work well and would make most people happy.

Plus people would still upgrade to new watches periodically to get the better hardware and screens, etc.

Then they could turn their focus to style, design, and use case. Like beauty vs battery life, etc.

not a bad idea but it just isn’t going to happen

If they sorted their software issues things would be a lot easier for them . The 955 / 255 have been a real disaster with bugs all over the place , terrible FW releasing etc . This is turning people off , even those who have been loyal to Garmin for decades!

what bugs were affecting you?

i was generally happy with it. bit of a lack of robustness with ciq (but that could be the ciq df) and my freakin screen is scratched. but apart form that….

Based on my understanding of Margin, 49% is massive, so I don’t see how that can be a bad thing. Companies struggle to get double digit margins in general.

Year over year is tricky with COVID boom in things like bike trainers, right?

that level of gross margin is healthy

the issue here is that Garmin and the markets have a shared expectation of the current levels of margins. once companies’ fortunes change and they can’t meet expectations then share prices will move more than you or I might expect.

margin after all costs is also important

so if you have a 51% gross margin and a 1% net margin (not the case with Garmin) if your net margins fall below zero you start eating cash and are loss-making. eg that could happen if the gross margins fall to 49%