Source: Shipment data from Counterpoint

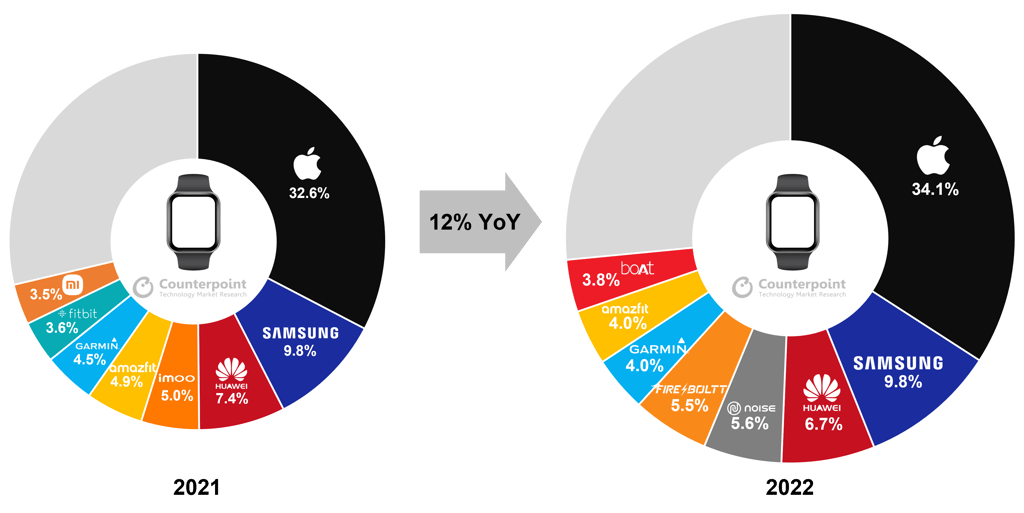

Garmin’s Share of Watch Shipments Declines in 2022

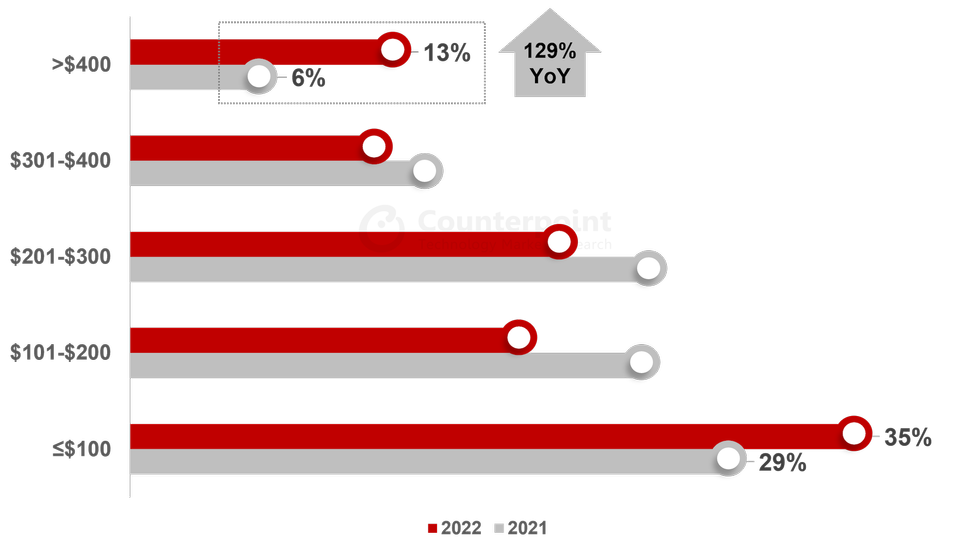

The trends in mid-market smartwatch shipments (B2B/trade sales) are causing significant concerns for smaller players as the smartwatch industry experiences polarized growth in 2022, as evidenced by Counterpoint’s research data comparing 2022 with 2021.

According to the chart, there is a decline in the importance of smartwatches priced between $100 and $400, with the red bars indicating snowballing growth at the over $400 and under $100 price points. This suggests that competition at the mid-tier price point should intensify, posing a challenge for smaller players.

What is driving this and who benefits?

The cheaper sub-$100 watches are ones that do not generally allow 3rd party apps and these are the ones that are riding on a wave of first-time demand in relatively new, less developed markets like India. This site focuses on competent sports watches and there are virtually none in this price tier.

However, the decline in shipments is not consistent across the board and we can see that the high-end watches have increased in sales. I would agree with Counterpoint in that this is closely linked to the impact of the Apple Watch Ultra as we see a bigger overall market compared to 2021 and a bigger share of it from Apple.

Fitbit seems to have entirely crashed out of the picture as Garmin’s market share also heads in the wrong direction, down from 4.5% to 4%. We recently saw the impact of this in Garmin’s 2022 financial reports.

Perhaps the main drivers for the current woes are:

- Overall low-end growth is driven by sales to wholly new customers eg in India

- Pent-up demand released for more sports-capable Apple Watches (Ultra)

- In recent years Garmin has constructed a market justification for high-end sports watches that are fully featured in quality shells.

- Recessions fears in many countries

Take Out

I’ve been periodically banging on about the ‘fact’ that only high-margin/low-volume and low-margin/high-volume products will see success in the smartwatch market in the long term. In 2022, this view seems to be more clearly seen, which is a significant cause for concern for smaller industry players who only compete effectively in the mid-market.

Companies such as Fitbit, Polar, Wahoo (Rival), and Suunto are probably in difficult positions as competition increases, squeezing their sales out from above and below. Apple and Garmin appear to be well-positioned at the upper end of the market; however, they both play significant roles at the mid-tier price level. They will also suffer there, but they are perhaps better positioned than most to weather the ongoing financial storm.

However, what I suspect will happen in the mid-tier is more subtle. Apple has a pseudo-monopoly by virtue of deep iOS integrations and should easily be able to maintain a credible business with Watch 8/SE gen 2. With Apple, customers simply opt for the cheaper SE or more expensive Watch 8 option and then fiddle around with colours, straps, and finishes. But Garmin can’t help itself from confusing customers with a plethora of sub-brands and complex feature differences. Garmin cannot change this, the confusion is inherent to its fundamental model of deep product differentiation.

To put it another way, Garmin’s mid-tier business is up for grabs to a savvy competitor. Unfortunately, that competitor is probably only Apple (or Google/Fitbit/Samsung) in the longer run. Garmin will always be able to differentiate itself at higher price points with an unbeatable range of sports features. Maybe that’s where its future lies. But low volume + high value = a different company.

Last Updated on 27 January 2026 by the5krunner

My favourite kit and nutrition

- Injinji – Runners protect your toes. Avoid discomfort and minor injury. Run more. run faster. I use them.

- Garmin 90-degree charging adapter — the small adapter that keeps your charging cables tidy. Essential for race day. I use one.

- Garmin charging puck — the fastest and most reliable way to top up your Garmin before a session. I use one.

- Ravemen FR300 — front light that mounts directly under your Garmin or Wahoo head unit. Keeps your bars clean and your beam pointed where it matters. I use one.

- Body Glide – The Blue anti-chafe stick that all swimmers and many runners use. I use it.

- Maurten — the race nutrition trusted by elite athletes. Gels and drink mix engineered to be easy on the stomach. I use them.

- Garmin Varia RTL515 — radar rear light that alerts you to vehicles approaching from behind. Pairs with your Edge or Garmin watch. I use this model.

- Favero Assioma Pro RS2 — the power meter pedals most serious cyclists end up choosing. Accurate, easy to move between bikes. I use this model.

Reader-Powered Content

This content is not sponsored. It’s mostly me behind the labour of love, which is this site, and I appreciate everyone who supports it.

Support the site: Follow (free, fewer ads) · Subscribe (paid, ad-free) · Buy Me A Coffee ❤️

All articles are written by real people, fact-checked, and verified for originality. See the Editorial Policy. FTC: Affiliate Disclosure — some links pay commission. As an Amazon Associate, I earn from qualifying purchases.

tfk is the founder and author of the5krunner, an independent endurance sports technology publication. With 20 years of hands-on testing of GPS watches and wearables, and competing in triathlons at an international age-group level, tfk provides in-depth expert analysis of fitness technology for serious athletes and endurance sport competitors. ID

“Analysists”.

I’m not sure that I believe the market analyst data. We are to believe that Amazfit, FireBoltt, and Noise all outsell Garmin?

The “units shipped” number is a huge hedge. For Apple, who famously operate just in time manufacturing the units shipped should closely track to the units sold and probably the same for Garmin. On the other hand Noise might build a run of something that does not sell and then have to slash the prices to try to clear the stock. But those are still “shipments”.

Famously Apple does not share unit sales information or even break out watches from AirPods and other accessories, so where do these numbers even come from?

What even defines a smartwatch?

FireBolt and Noise are apparently only sold in India. I just went to fireboltt.com and the top watches they promote are between 1400 rupees and 3500 rupees. That is <$20 to <$45. I do not believe these are even the same market of thing. Nobody considering an Apple Watch or a Garmin is going to buy a FireBoltt instead.

Noise and FireBoltt both claim to be the #1 smart watch brand of India!

I think there is a lot of fudging in these graphs in a way that makes them meaningless.

I believe that Apple sells more watches than Garmin. The absolute quantities seem speculative. I’m not even sure I believe that Samsung is in between.

Strictly anecdotal but I have seen one Hwawei watch and one amafit watch in the real world across 3 continents in the past 3 years. Not Asia, though, which is probably the stronghold. I was hanging out with a Korean diplomat runner and his watch was a Garmin. N of 1.

I used to work in the area of ex-factory data and there are various ways to get fairly accurate market share info (sometimes precisely accurate!).

this market research company have been around for years, so i hope whatever methodology they use is consistent over time.

shipment/trade sales are not retail sales.

yep anecdotal evidence requires you to hang out with a wide range of representative people.

Garmin should have more models with LTE. Lack of LTE is stopping most of the potential costumers from buing Garmin watches. Why is garmin not aware of this?! I would like to see constructive response. With latest apple watch pro and galaxy 5 pro, one can go without the phone on the ski or the bike trails almost on whole day on LTE! Thats important step forward. Where is Garmin at this point? Garmin, the company long before them. They will loose market share year by year.

hey there.

ATM, i use apple watch 7 lte. it can do about 5 hours of GPS recording with LTE on. when not recording GPS then maybe i can get a good day out of LTE (with no LTE it lasts over a day). it’s handy for me for an emergency phone call when cycling and easier to use than getting a phone out of my back pocket.

i don’t think lte is as popular as you imply (I could be wrong)

garmin has delivered other services over lte already.

however, garmin will not be able to deliver voice calls over lte.

garmin just won’t be able to integrate as deeply as apple watch on iOS and if it wants to integrate deeply on android then i would assume it has to go for Wear OS…and then the battery issues will come back to spoil the party.

from memory, i think the garmin venu CAN make calls with its microphone. however, it’s doing it over Bluetooth via the smartphone in your back pocket. to introduce a similar feature in a sports environment raises other issues like 1) people might not want to carry a phone when they exercise 2) adding a mic/speaker adds more challenges for water resistance.