Polar now Supports 3rd Party Electronic Payments

Polar now Supports 3rd Party Electronic Payments

6 months ago I heard a rumour, later corroborated, about Polar getting into payments with its watches. Suffice it to say I was extremely sceptical of the information. The essence of my scepticism was, “How can Polar hope to succeed where Garmin has only managed to complete half of the same job?”

via: lots of people, thank you all!

How Garmin and Apple Support Card Payments

When Apple stores your credit or debit card on its devices instead of storing your card number it stores an encrypted and secure token.

During a transaction and after you have passed biometric checks (pin code, face check) that token is combined with the sale details into a cryptogram. The token and cryptogram are both sent to the payment processor who in turn sends it to the card network (AMEX/Visa). The card network then passes the information to the organisation that issued the card to you (Santander, Lloyds, Sainsbury, etc) and approval is granted if you have funds. The approval is passed back down the chain, various other checks are made and if all is good you get to walk away with your purchase.

Garmin follows the same processes.

More: Detailed Polar Grit X2 Pro Review

However the difference, to me, seems to be that Garmin has had to negotiate arrangements with every card issuer, whereas Apple seems to have agreements at the card network level.

The Mountain Polar Had to Climb

Perhaps this section should be entitled, “The Mountain I Thought Polar Had To Climb”.

Presumably, Garmin is not big enough to negotiate on the same level as Apple with far fewer annual transactions. Rather than dealing with a small number of card networks, Garmin dealt with many card issuers. The bottom line for you as a Garmin owner is that Garmin has only had limited success there and it is a lottery if your bank (card issuer) is one of the ones covered by Garmin’s agreements.

By a similar argument linked to corporate size, Polar is much smaller than Garmin and hasn’t even the means to negotiate the number of deals as Garmin. From the other side of such agreements, many card issuers won’t be interested in talking to Polar due to low transaction volumes.

So I (wrongly) assumed this was the mountain that could not be climbed. I guess you could take the funicular or go through the tunnel tough, right? you don’t have to climb it. (to continue the metaphor)

More: Detailed Polar Vantage V3 Review

Roll In Fidesmo

Fidesmo is similar in scope to Apple Pay, although smaller. Fidesmo mostly focuses its financial agreements on VISA and MASTERCARD networks (but not AMEX) and also works with a digital wallet called CURVE plus other organisations.

Once you join Fidesmo, you load your (tokenised) card details and Fidesmo handles the transaction on an individual, instant basis with your card issuer, following the same kind of process outlined earlier.

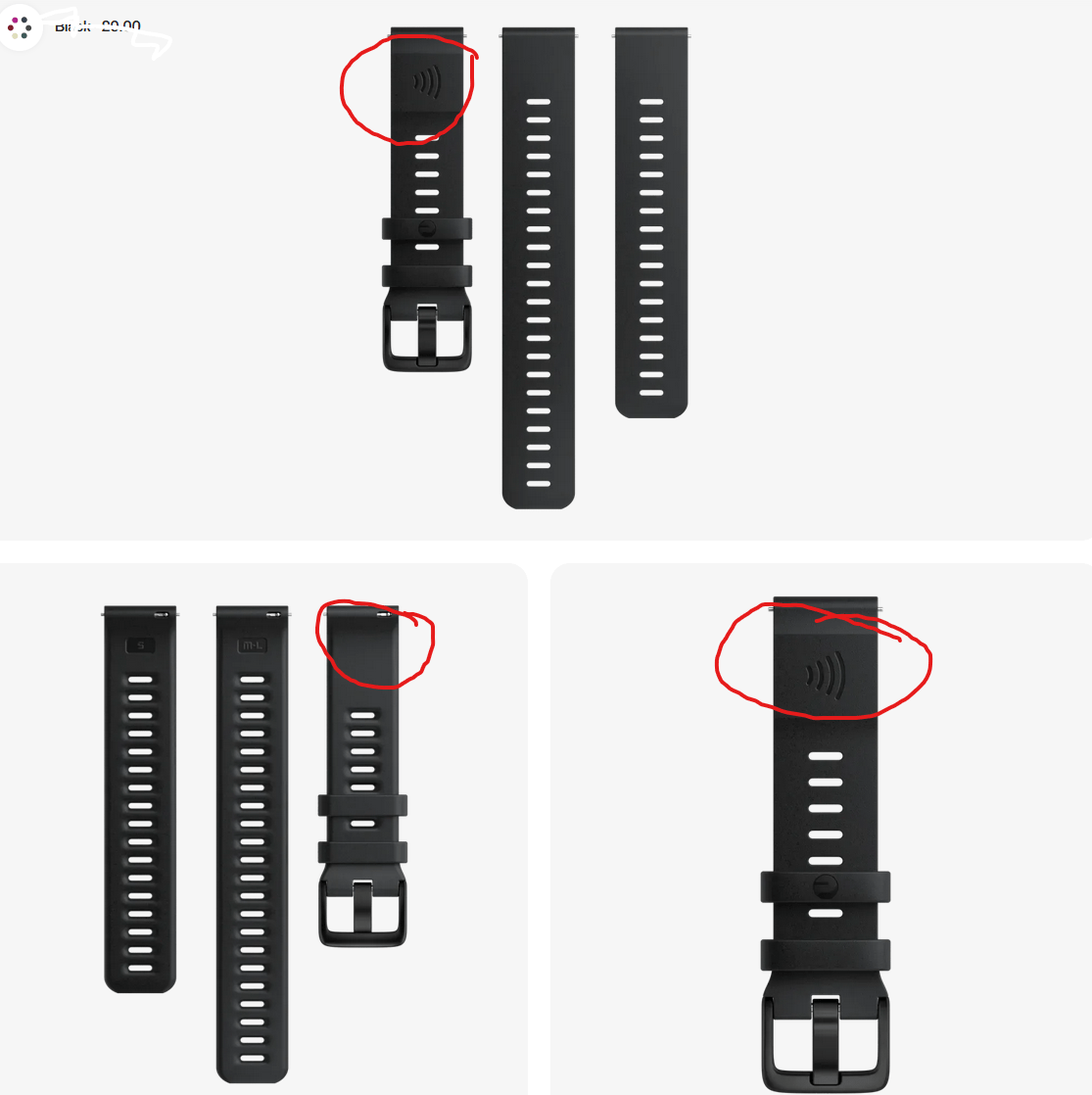

The key difference is that Fidesmo also produces a piece of NFC hardware which effectively stores your token and that token can only be used with the Fidesmo hardware its installed on (NFC Chip).

Fidesmo integrates its chips into other devices, typically physically locating them on the outside of wearables rather than inside them.

Thus Polar has Fidesmo integrated into a standard-width watch band.

Voila!

You could quite easily add Fidesmo to a key, a piece of jewellery or a watch. And that’s precisely what Polar has done.

Is It As Secure as Apple Pay?

A: Well. I’d say NO. Fidesmo disagrees.

Sure, the tokenisation process is the same as Garmin or Apple use. In that sense it is secure. However, with Fidesmo integrated into a watch strap, there isn’t any biometric checking for each transaction. Thus if you lose your watch or have it stolen, assuming the thief knows what they have, they can then go on to illegally use it.

There are mechanisms for you to quickly and easily cancel the token (here), however, they all assume that you realise you’ve lost your watch or had it stolen and that you have access to the means of cancellation.

On the other hand, the theft or loss of a physical credit card carries the same risk of misuse by a thief.

Note: Other companies are working on biometric authentication using unique patterns in heart rate signatures. One day that could be integrated into a Polar strap but that day is not today.

Would I use This?

A: Probably Not

I use Apple Pay and don’t carry my credit cards around with me…nor cash for that matter.

I occasionally use a Starling Bank account with Garmin PAY protected with a PIN code. Even if PIN-level security was breached by a thief, the account has very limited funds that I use for purchases of coffee and cake.

How to Guide: use Garmin PAY with most banks – here

Polar Payments – Take Out

Despite my negativity in the last two paragraphs, this is a good move from Polar and one which other wearable companies can take up equally as easily. Heck, you could even use the standard-width Polar bands as a replacement for ANY generically sized watch strap.

Polar has ticked off another of the key boxes on the checklist of must-haves for sports and wellness wearables. Let’s hope that those who use the Fidesmo service via Polar use some caution.

Looking wider than that, this is another move that shows Polar is thinking outside of the box it seemed to have gotten into over the last decade. It will never win by playing Catch-Up to Garmin. So now Polar is innovating and licencing access to its ecosystem and algorithms, as well as providing payment services.

Nice job. With reservations.

User Poll – Have Your say

It’s not looking good though…

Would you trust your credit card payment details to a secure NFC chip watch strap with no biometric authentication? https://t.co/R5WeXE9bgf

— the5krunner (@the5krunner) May 16, 2024

Last Updated on 28 January 2026 by the5krunner

My favourite kit and nutrition

- Injinji – Runners protect your toes. Avoid discomfort and minor injury. Run more. run faster. I use them.

- Garmin 90-degree charging adapter — the small adapter that keeps your charging cables tidy. Essential for race day. I use one.

- Garmin charging puck — the fastest and most reliable way to top up your Garmin before a session. I use one.

- Ravemen FR300 — front light that mounts directly under your Garmin or Wahoo head unit. Keeps your bars clean and your beam pointed where it matters. I use one.

- Body Glide – The Blue anti-chafe stick that all swimmers and many runners use. I use it.

- Maurten — the race nutrition trusted by elite athletes. Gels and drink mix engineered to be easy on the stomach. I use them.

- Garmin Varia RTL515 — radar rear light that alerts you to vehicles approaching from behind. Pairs with your Edge or Garmin watch. I use this model.

- Favero Assioma Pro RS2 — the power meter pedals most serious cyclists end up choosing. Accurate, easy to move between bikes. I use this model.

Reader-Powered Content

This content is not sponsored. It’s mostly me behind the labour of love, which is this site, and I appreciate everyone who supports it.

Support the site: Follow (free, fewer ads) · Subscribe (paid, ad-free) · Buy Me A Coffee ❤️

All articles are written by real people, fact-checked, and verified for originality. See the Editorial Policy. FTC: Affiliate Disclosure — some links pay commission. As an Amazon Associate, I earn from qualifying purchases.

tfk is the founder and author of the5krunner, an independent endurance sports technology publication. With 20 years of hands-on testing of GPS watches and wearables, and competing in triathlons at an international age-group level, tfk provides in-depth expert analysis of fitness technology for serious athletes and endurance sport competitors. ID

Today my Polar/Fidesmo Strap arrived. First I have to say that this is of excellent quality! Soft and strong material, very comfortable to wear. And a innovative adjustment of the keepers – I‘m very happy with that.

The pay functionality is very good. Only the configuration (especially sending the card information to the NFC chip) is a bit challenging. It is important to read the instructions carefully and follow them step by step.

After you are through with this you have both: A premium watch strap that is good for any condition and a smart way to pay (especially daily little amounts). Well done Polar!!!

Glad to hear you are happy with it! Let us know the experience as i don’t have plans to review it

That strap looks like I can use it with my pace 3 as well. That would be nice. Any technical reason it won’t work with a non Polar watch?

nope. as long as it fits it will work

you’ll probably need to get a CURVE account…but thats no biggie. they are just a conduit for your payment from your existing bank and dont hold a balance.