Garmin Q1 2026 Earnings: Fitness Up 42%, Fenix (-5%) has a problem, Share Price Slips

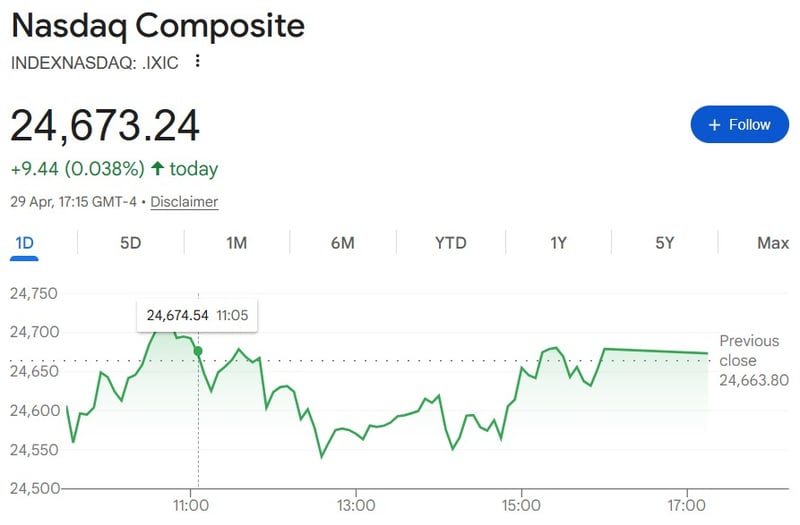

Garmin opened 2026 with record first-quarter revenue, double-digit growth in three of five segments, and meaningful margin expansion across the business. The market response was tepid. At the time of writing, GRMN was down 1.61% against a NASDAQ fall of just 0.15%; subsequently, both rose, but still painted a similar picture.

Relative declines are often due to a failure to meet expectations, and the likely candidate here was the declining performance of the Outdoors Division, home of the Fenix and the historical cash generator for Garmin, which held a once-unassailable competitive position.

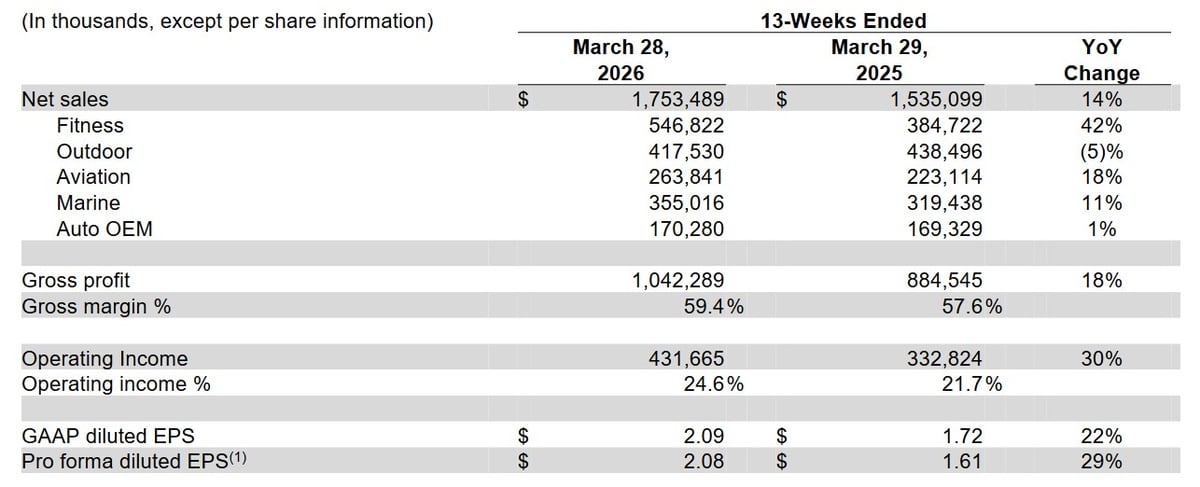

Fitness: Revenue increased 42% to $547 million, which is a new first-quarter record driven by broad-based growth across all product categories, led by strong demand for advanced wearables. The primary driver of our performance is higher unit volumes, resulting in meaningful market share gains… we expect that the fitness segment will be the strongest contributor to 2026 consolidated growth. [Pemble]

Fitness: Revenue increased 42% to $547 million, which is a new first-quarter record driven by broad-based growth across all product categories, led by strong demand for advanced wearables. The primary driver of our performance is higher unit volumes, resulting in meaningful market share gains… we expect that the fitness segment will be the strongest contributor to 2026 consolidated growth. [Pemble]- Outdoor: Revenue decreased 5% to $418 million as we compared against a strong prior year quarter, which included the launch of the Instinct 3 smartwatch family. Fenix smartwatches performed well during the quarter, even considering the strong comparable from the prior year… we expect to achieve stronger performance in the back half of the year due to the timing of product launches. [Pemble]

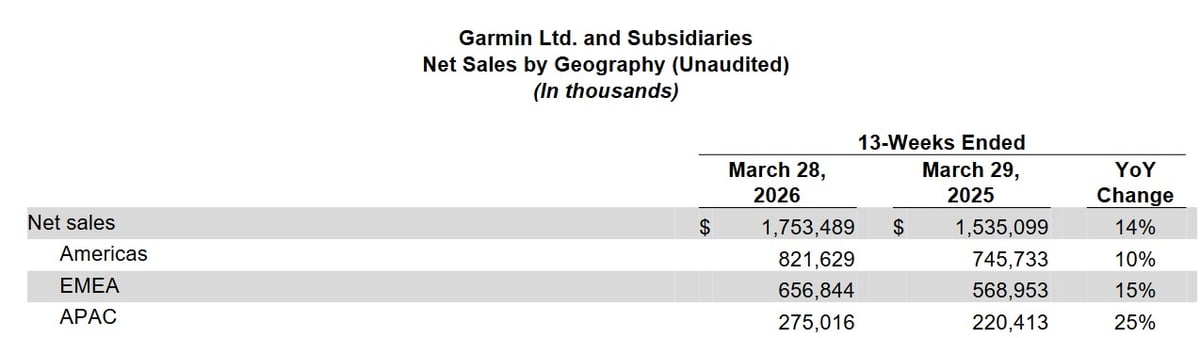

Geographically, Q1 strength was led by APAC at 25% growth, followed by EMEA at 15% and the Americas at 10%. Both EMEA and APAC benefited from favourable foreign-currency movements. The pattern broadly inverts in Q4 2025, with the Americas leading at 21% and APAC trailing at 8%.

Garmin’s cash position continued to build, ending Q1 with cash-like assets of approximately $4.3 billion, up roughly $200 million on the Q4 close. Free cash flow for the quarter was $469 million, $9 million higher than Q1 2025. The company paid $174 million in dividends and bought back $40 million of stock during the quarter, with $491 million remaining on the share repurchase programme through December 2028.

Against Expectations

The disconnect between Q1 results and Q1 share price reaction is the story of this quarter. Pro forma EPS of $2.08 represented a 29% year-on-year gain. Operating margin of 24.6% expanded 290 basis points. Three segments delivered first-quarter records. By any standard reading of an earnings release, this was a strong performance.

The market response told a different story. Three factors appear to be in play.

- First, management held full-year 2026 guidance flat at the figures issued in February, declining to raise on the strength of Q1. Pemble explicitly framed the quarter as a single data point in what is typically Garmin’s lowest seasonal period, telling analysts that “much of the year remains ahead.“

- Second, the share price had already entered the call elevated following the Q4 surge, leaving limited room for further re-rating.

- Third, investors were primed by the Q3 2025 outdoor stumble to look for weakness, and a second consecutive soft outdoor quarter gave them what they were looking for.

These charts were captured a day after the results were announced. Results were announced at 7:30 Eastern. The subsequent rise trailed the market. Again, a relative decline.

My Personal Take: The Q4 surge corrected an earlier mispricing. Today’s modest decline from Q1 figures looks like consolidation or blip rather than a verdict on the quarter itself. The numbers are strong and Pemble expressed strength looking forward. The market simply needed more than strong to push higher from current levels. Garmin’s long-run trajectory remains intact.

Fitness as the Engine: Volume-Led Market Share Gains Continue

The Fitness division is now unambiguously the centre of gravity at Garmin. Q1 revenue of $547 million represented 42% year-on-year growth, the same headline rate posted in Q4 2025. Pemble was explicit that growth was driven by higher unit volumes rather than price. This is the same pattern that defined Q4. Garmin is taking share by shipping more devices in a market that is itself expanding.

The competitive backdrop matters here. Asked directly by JP Morgan about the rise of subscription-based and hardware-as-a-service wearable competitors (a la Whoop), Pemble responded that customers want choices in the devices they wear and that Garmin remains “open to all kinds of devices and form factors in how we deploy our wearable sensor technology.” Read alongside his closing remark that 2026 will see launches “that represent new categories for Garmin,” the Fitness division’s dominance looks likely to broaden, not narrow. The expected CIRQA launch is one component of that. Pemble’s use of the plural strongly suggests it is not the only new product area.

A second strategic thread worth noting: Pemble described subscription services as “an area of enhanced focus” for Garmin, citing Connect+ alongside subscription offerings in other segments. The phrase “enhanced focus” implies more is coming. Strength training programming, advanced coaching modules, or further AI-led features within Garmin Active Intelligence would all fit the description.

Note: None of these new product areas will be news to regular readers. We’ve been covering them for months – CIRQA, Strength ecosystem, SMO2 sensors, HUDs.

For the full picture on what CIRQA is expected to do, its likely price, and how it sits against Whoop and Fitbit Air, see Garmin CIRQA: Everything We Know.

What’s Coming Next

Two signals point to Garmin product launches landing within weeks rather than months. The first is Pemble’s reference to 2026 launches that represent new categories for Garmin. The second comes from outside the earnings call entirely. DC Rainmaker, the most prominent independent reviewer in the wearables space, has begun posting Strava activities from Olathe, Kansas, the location of Garmin’s headquarters. That pattern almost always indicates an embargoed product briefing. The window between an Olathe visit and a launch is typically two to four weeks.

The leading candidate remains the CIRQA arm-worn band, which would put Garmin into direct competition with Whoop and the rumoured Suunto SHRM2. Pemble’s use of the plural in “new categories” suggests CIRQA is not the only product on the runway. Strength training hardware, an SMO2 sensor, and a head-up display product have all surfaced through the5krunner’s reporting in recent months.

A separate strategic shift is also visible. Leaked Garmin Connect app code points to a Strava-like rebuild of the social layer, with mutual follows reframed as friends, follow requests introduced, and contact-based discovery added. Read alongside Pemble’s framing of subscription services as an area of enhanced focus, the path to a Connect+ tier that competes with Strava’s social and segment features begins to take shape. Full analysis of Garmin’s Strava ambitions is here: Garmin vs Strava: Leak Shows Connect Targeting Strava.

Outdoor: A Second Consecutive Soft Quarter

Outdoor revenue declined 5% to $418 million, the second consecutive quarter of weakness following Q4 2025’s flat result and Q3 2025’s 5% decline. The Q1 comparable was tough by design, with the year-ago quarter including the launch of the Instinct 3 family. Pemble was at pains to note that Fenix smartwatches “performed well during the quarter, even considering the strong comparable,” which reads as a deliberate effort to head off concerns that the momentum of the Fenix 8 Pro has stalled.

The more material commentary was forward-looking. Pemble told analysts to expect “stronger performance in the back half of the year due to the timing of product launches, resulting in improved full-year growth when compared to 2025.” Translation: significant Outdoor product launches are scheduled for H2 2026. Whether that means a Fenix 9, a refreshed Instinct line, a new Tactix, or something else entirely, the second half of the year is when the Outdoor recovery is expected to land.

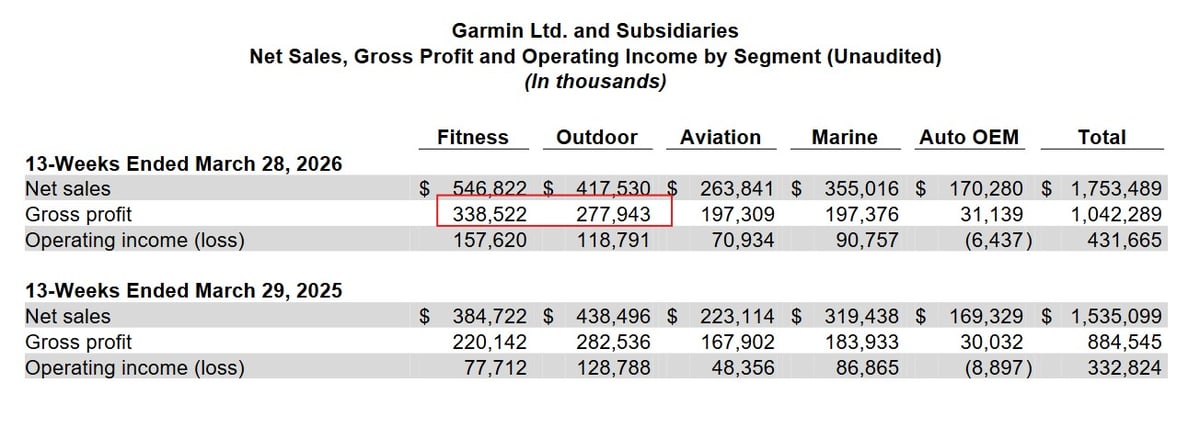

Outdoor’s gross margin held firm at 67%, second only to Aviation across the business. The weakness is volume-driven rather than the result of competitive pricing pressure.

Positive Note: If ever it were needed, this is the impetus for Garmin to give us the best possible Fenix 9 they can. Roll on Q3!

Key Takeaways for Garmin’s Future

- Fitness continues to set the tone. A second consecutive quarter of 42% growth confirms that the Fitness division is structurally driving Garmin’s results. The volume-led nature of that growth, with market share gains explicitly called out, is more important than the headline number.

- New categories are coming. Pemble’s closing remark that 2026 will see launches “that represent new categories for Garmin” is the most consequential single line of the call. The CIRQA Whoop competitor appears to be the leading candidate, but Pemble’s use of the plural suggests more than one such product in the pipeline.

- Garmin is moving on Strava. Leaked Connect app code points to a follower-based social rebuild, and Pemble’s “enhanced focus” on subscriptions provides the commercial vehicle. Connect+ as a platform open to non-Garmin workout data, with physiological computation reserved for Garmin hardware, is the most plausible competitive shape. Full analysis is here.

- Subscription is being elevated. The phrase “enhanced focus” applied to subscription services signals further development of Connect+ and likely additional subscription tiers across the product range. Strength training programming is one plausible direction.

- Component cost pressure is deferred, not avoided. CFO Doug Boessen confirmed that current results are insulated by safety stock, with cost increases expected to begin flowing through in 2027. Garmin pricing is likely to rise next year.

- Outdoor needs H2. Two consecutive soft quarters are a pattern. Pemble’s commitment to back-half product launches is now load-bearing for the full-year Outdoor narrative.

- Guidance held, not raised. The decision to maintain February’s full-year guidance despite a strong Q1 is consistent with Garmin’s historic conservatism. It is also what costs the share price today. A Q2 raise would change that calculus.

Sources & Resources

Garmin Q3 2025 Earnings: Fitness Explodes, Fenix 8 Pro Underwhelms

explosive Garmin Q2 Earnings – significant Forerunner 970 contribution (2025)

For the complete Garmin Fenix series guide, covering all current models, history and buying advice: Garmin Fenix hub.

Last Updated on 31 May 2026 by the5krunner

My favourite kit and nutrition

- Injinji – Runners protect your toes. Avoid discomfort and minor injury. Run more. Run faster. I use them.

- Garmin 90-degree charging adapter — The small adapter that keeps your charging cables tidy. Essential for race day. I use one.

- Garmin charging puck — the fastest and most reliable way to top up your Garmin before a session. I use one.

- Ravemen FR300 — Front light that mounts directly under your Garmin or Wahoo head unit. Keeps your bars clean and your beam pointed where it matters. I use one.

- Body Glide – The blue anti-chafe stick that all swimmers and many runners use. I use it.

- Maurten — The race nutrition trusted by elite athletes. Gels and drink mixes engineered to be easy on the stomach. I use them.

- Garmin Varia RTL515 — A radar rear light that alerts you to vehicles approaching from behind. Pairs with your Edge or Garmin watch. I use this model.

- Favero Assioma Pro RS2 — The power-meter pedals most serious cyclists choose. Accurate, easy to move between bikes. I use this model.

- Garmin Forerunner 970 — A serious choice for a pro-grade triathlon watch. I use this.

- Polar H10 — My daily driver for accurate, waking HRV readings.

- Wahoo ELEMNT Roam 3 — The bike computer that has the feature Garmin lacks: usability. I use mine on most rides.

Reader-Powered Content

This content is not sponsored. It’s mostly me behind the labour of love, which is this site, and I appreciate everyone who supports it.

Support the site: Follow (free, fewer ads) · Subscribe (paid, ad-free) · Buy Me A Coffee ❤️

All articles are written by real people, fact-checked, and verified for originality. See the Editorial Policy. FTC: Affiliate Disclosure — some links pay commission. As an Amazon Associate, I earn from qualifying purchases.

tfk is the founder and author of the5krunner, an independent endurance sports technology publication. With 20 years of hands-on testing of GPS watches and wearables, and competing in triathlons at an international age-group level, tfk provides in-depth expert analysis of fitness technology for serious athletes and endurance sport competitors. ID

Small correction: “Garmin’s cash position weakened slightly” is incorrect. The cash position actually stayed the same – and improved by $87m when taking into account marketable securities:

Cash and cash equivalents $ 2,072,208 $ 2,079,468

Marketable securities 515,038 421,270

The table/exhibit you posted is not cash position (which is a balance sheet item) but rather for (free) cash _flow_ during the period. And even then, the decline in free cash flow is quite benign because it is mostly due to a significant (> $200m) net increase in inventories – no doubt connected to the new device launches and in order to avoid OOS situations, like noted for the FR970.

If you go to Garmin Forums and compare the comment sections of the 570 and 970, it’s staggering….either the 570 is perfect out of the box with no bugs whatsoever…or no one is buying it….I suppose the latter.

But it seems the the Sleep Index Band has been delivered to the early adopters, because the first complain are coming in…Did you get one? I wonder how much the band data will deviate from the watch data.

in the context of this artcile i dont know how garmin books its revenue

it could invoice trade buyers of Index as it ships bulk volumes

i dont plan to get one. but i might eventally. if it was designed for sport i would

Could be that there’s no shortage of people who owned Fenix 6 and 7 series, as well as the Epix, ditching Garmin for other manufacturers thanks to their antisocial update policy.

Hilarious. They think that locking more features behind a subscription paywall connect + is a good way forward. I will literally buy a Coros watch the moment I feel they have crossed the line. Consumers have had enough of the endless subscription services and are scaling back. Build it into the price of the device but NO MORE SUBSCRIPTIONS.

It IS built into the (premium) price of the device, we all know that. Yet Garmin has to have a decent base subscription revenu stream to survive in the very long term – as this article argues: https://the5krunner.com/2026/05/05/garmin-empire-crumble-when/

It has to walk a precarious tightrope that is wobbling quite a bit