Strong Q1 Earnings from Garmin

Strong Q1 Earnings from Garmin

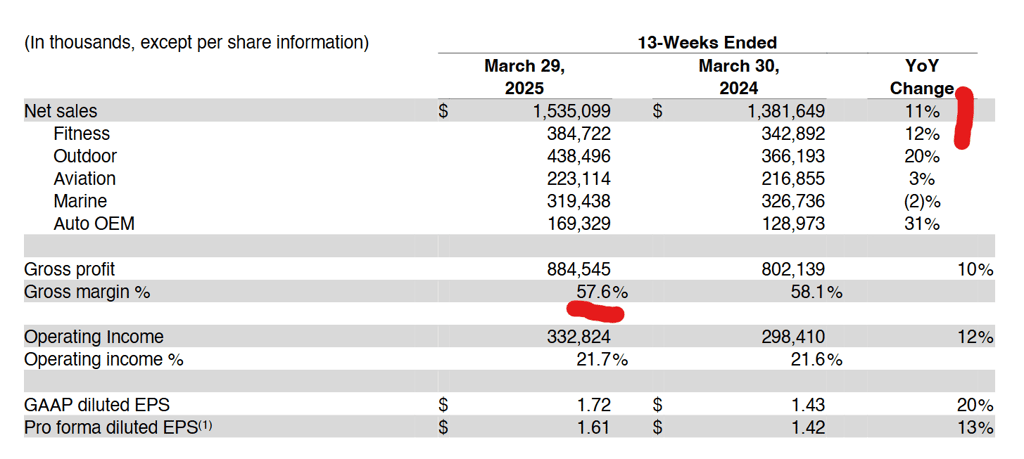

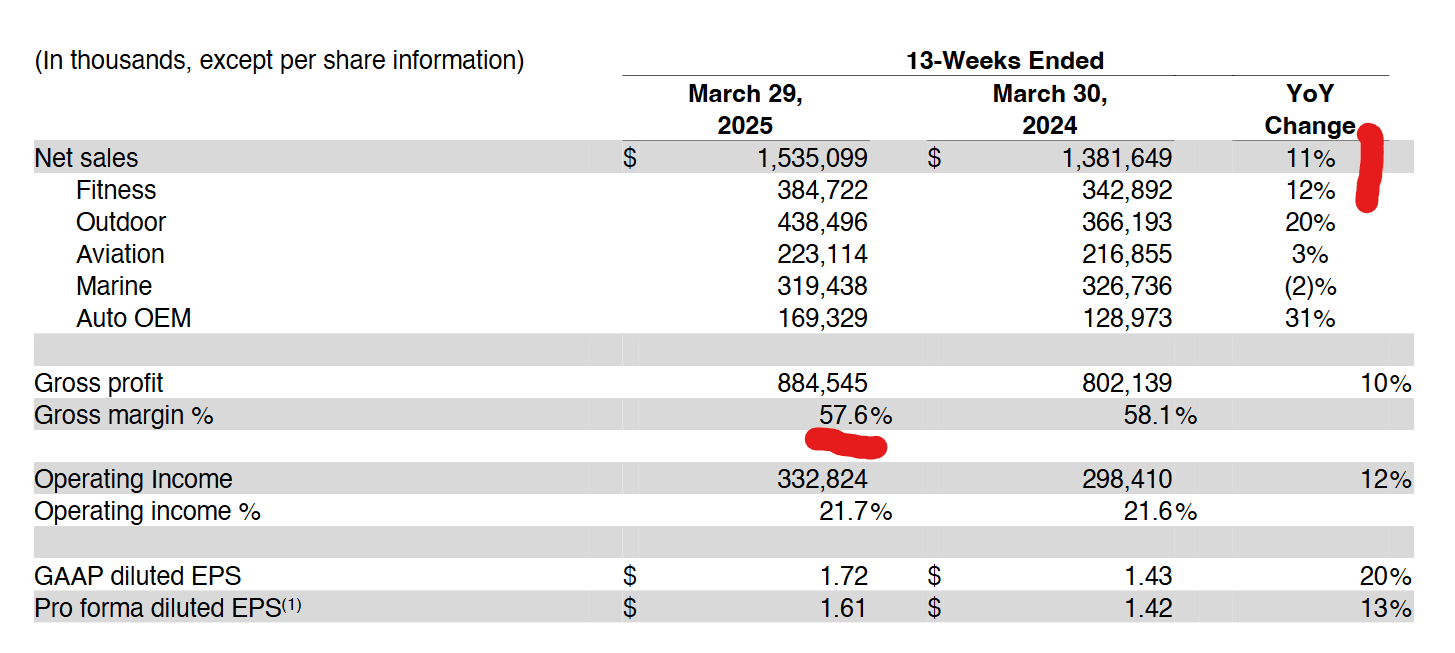

The latest quarterly stats from Garmin show sales in the Fitness (Forerunner, Edge) and Outdoor (Fenix) divisions grew nicely year-on-year, with its profitability at about the right levels.

We delivered another quarter of outstanding financial results which we attribute to our strong lineup of highly differentiated products that customers desire. While recent developments in global trade have created an

atmosphere of uncertainty for many companies, we remain optimistic because of the resilience and flexibility our vertically integrated and highly diversified business model offers. We are very pleased with our results so far,

and we look forward to the opportunities ahead as the year continues to unfold. [Pemble, CEO]

Pemble continued with more details that should interest regular readers here, and of particular note is the highly profitable outdoors business.

Revenue from the fitness segment increased 12% in the first quarter with growth led by strong demand for advanced wearables. Gross and operating margins were 57% and 20%, respectively, resulting in $78 million of operating income. During the quarter, we announced Garmin Connect+, a premium plan offering personalized insights driven by artificial intelligence, enhanced live tracking, and exclusive achievement badges. Garmin Connect+ will elevate users’ health and fitness knowledge with personalized Active Intelligence insights powered by AI…We also recently announced the vívoactive 6, our newest health and fitness smartwatch with an even brighter AMOLED display that includes more than 80 preloaded sports apps and provides access to Garmin Coach running and strength training plans.

Revenue from the outdoor segment increased 20% in the first quarter primarily due to growth in adventure watches. Gross and operating margins were 64% and 29%, respectively, resulting in $129 million of operating income. During the quarter, we launched several wearables, including Instinct 3, Descent G2, tactix 8 and Approach S44 and Approach S50. Each wearable is purpose built to allow our customers to participate in the activities that further their passions. Also during the quarter, we launched the new Montana handheld GPS series with optional SOS satellite communication capabilities, and the new Approach G20, the first GPS golf handheld with unlimited battery life in sunny conditions.

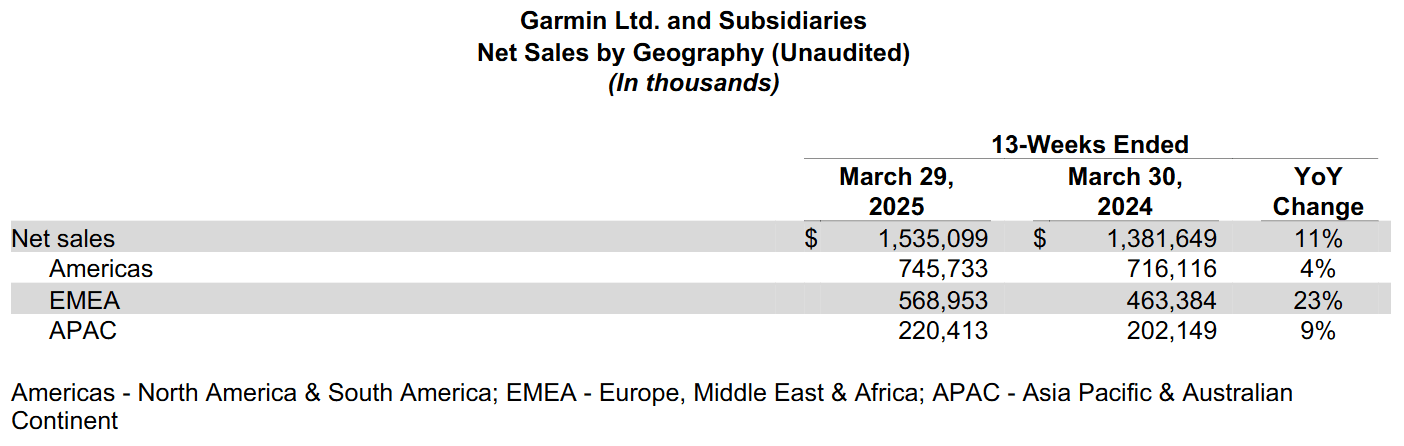

Looking at the various regional pictures, EMEA’s growth of 23% is good, albeit slightly lower than the 30% shown last quarter. Growth in the Americas is modest by Garmin’s standards and I would imagine that ne next wo quarters will be tricky for this region, and we might even see declines in Q3.

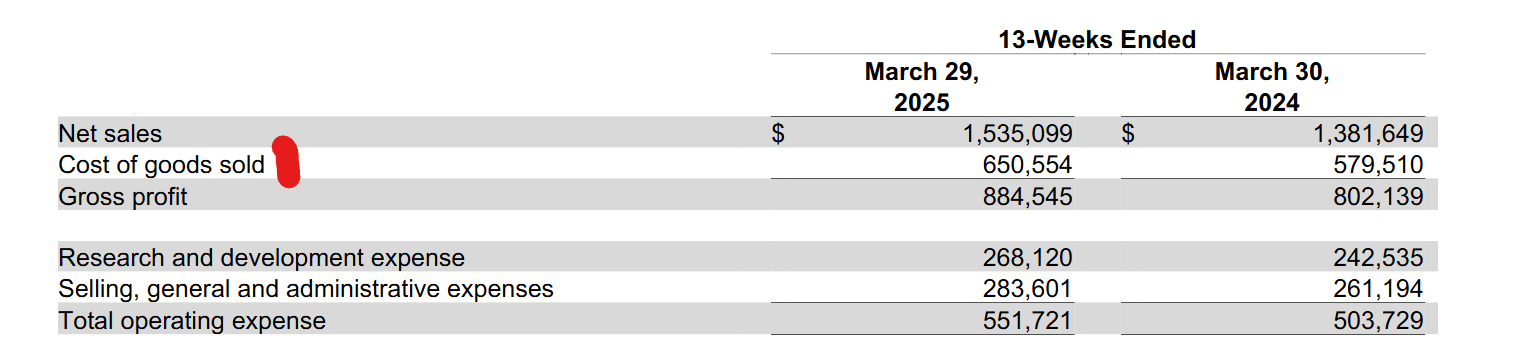

There is a significant increase in costs but that seems to reflect the associated costs wit increased sales rather than stocking up to avoid tariff issues.

I commented on the cash position 6 months ago. Still, it’s worth saying again that Garmin has $2bn of cash—enough to weather almost any economic storm.

Against Expectations

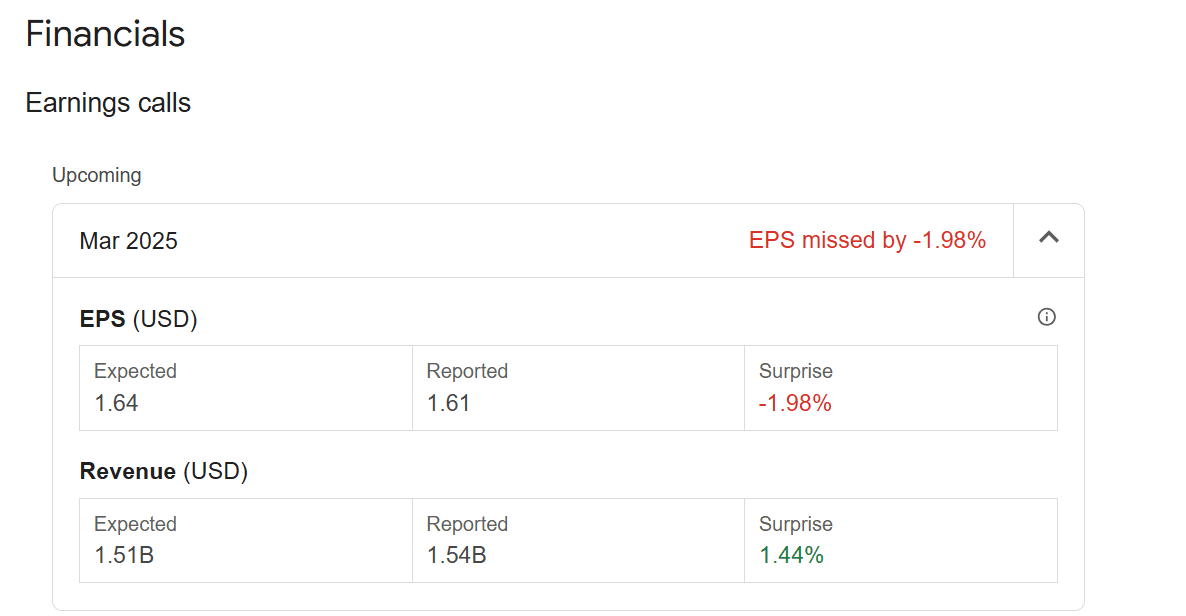

Good growth is one thing, but it only affects the share price if it differs from expectations. Bigger impacts on share prices are often from changes to forward-looking stats.

On the day Garmin released its financials, the NASDAQ, probably a better comparator than the NYSE, where Garmin is listed, fell by about 35 but Garmin’s shares fell by about a further 8%, which is significant.

These results were broadly in line with market expectations, except for missing EPS expectations.

Perhaps Garmin was perceived to be more impacted by whatever caused the adjustment of the NASDAQ? Indeed, it lowered forecast margin expectations. However, it did raise expectations for higher sales for the remainder of the year.

In a nutshell, it looks like the tariff wars and the uncertainty they create are at least one factor contributing to higher costs and a less certain outlook, but more positively, Garmin does not appear to plan to pass them on to consumers…at least not yet.

Take Out

Everything considered, that was good. the future looks more worrying.

Looking ahead to the remainder of Q2 and Q3, we can expect several significant product launches (FR975, FR275, Fenix 8 Pro, Edge 850), iterating previous models, new niche products (Varia vision), and new technologies (MicroLED, 4G LTE), potentially adding interesting revenue streams.

The macroeconomic conditions might suggest trickier times for Garmin, especially in the USA, but the company innovates with huge R&D budgets to give differentiated products that the top end of the market wants to buy. Garmin’s typical customer will likely be less squeezed than others.

Garmin Growth surprises the Market – Q3.2024 Earnings results are in.

Last Updated on 26 January 2026 by the5krunner

My favourite kit and nutrition

- Injinji – Runners protect your toes. Avoid discomfort and minor injury. Run more. run faster. I use them.

- Garmin 90-degree charging adapter — the small adapter that keeps your charging cables tidy. Essential for race day. I use one.

- Garmin charging puck — the fastest and most reliable way to top up your Garmin before a session. I use one.

- Ravemen FR300 — front light that mounts directly under your Garmin or Wahoo head unit. Keeps your bars clean and your beam pointed where it matters. I use one.

- Body Glide – The Blue anti-chafe stick that all swimmers and many runners use. I use it.

- Maurten — the race nutrition trusted by elite athletes. Gels and drink mix engineered to be easy on the stomach. I use them.

- Garmin Varia RTL515 — radar rear light that alerts you to vehicles approaching from behind. Pairs with your Edge or Garmin watch. I use this model.

- Favero Assioma Pro RS2 — the power meter pedals most serious cyclists end up choosing. Accurate, easy to move between bikes. I use this model.

Reader-Powered Content

This content is not sponsored. It’s mostly me behind the labour of love, which is this site, and I appreciate everyone who supports it.

Support the site: Follow (free, fewer ads) · Subscribe (paid, ad-free) · Buy Me A Coffee ❤️

All articles are written by real people, fact-checked, and verified for originality. See the Editorial Policy. FTC: Affiliate Disclosure — some links pay commission. As an Amazon Associate, I earn from qualifying purchases.

tfk is the founder and author of the5krunner, an independent endurance sports technology publication. With 20 years of hands-on testing of GPS watches and wearables, and competing in triathlons at an international age-group level, tfk provides in-depth expert analysis of fitness technology for serious athletes and endurance sport competitors. ID

1st quarter US GDP is negative growth and that is a lagging indicator of the damage from DOGE, tariffs, recision of federal spending, etc. Next quarter should be worse as the bill comes due, which is not good for anybody

you have to look at what makes up USA’s GDP. It has 4 or 5 key components one of which is imports. the basic growth in the non-import part of the economy is fine, there’s obvisouly been a massive uptick in imports.

so: the number is correct but the measure doesn’t account for the unusual situation ATM

who knows what the next quarter will be. I would imagine the import part falls off drastically (having a positive effect) but, yes, the consumer consumption side of things will fall. i’m an amateur economist but then most economists seem pretty rubbish at predictions.

I suggest everybody not reporting any bugs to Garmin until we see a disastrous quarter. 🙂

Right now it makes quasi zero sense.

Garmin doesn’t do great regardless how the 5krunner want to spin it…

“Garmin posted its slowest revenue growth in seven quarters and missed profit estimates on sluggish demand for its navigation devices and smartwatches…”

https://www.reuters.com/business/navigation-device-maker-garmin-misses-profit-estimates-shares-slump-2025-04-30/

you are right.

my share charts were from earlier in the day and must have lagged from before the annoucement. i will update

No company always grows, and not steadily.

That said I just hope that Connect+ is not profitable so Garmin reverts back on their decision. Time will tell