How Garmin’s Fitness Division Triggered a 20% Share Price Explosion in Q4 2025

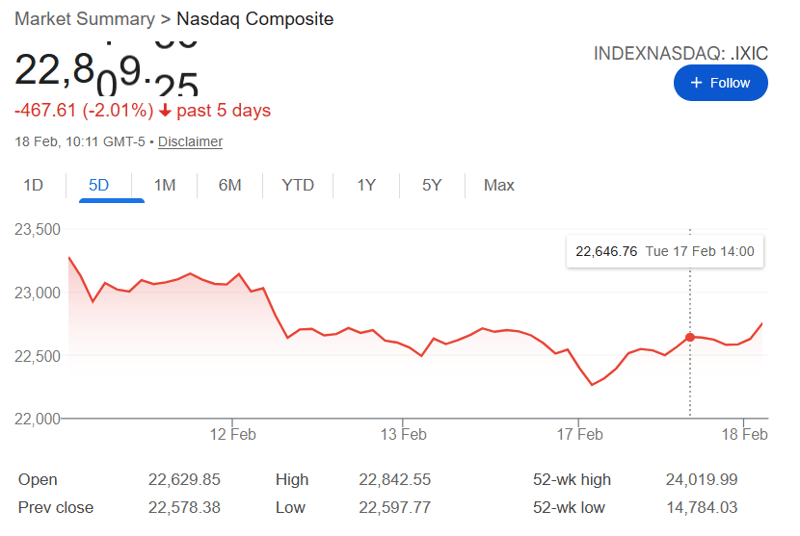

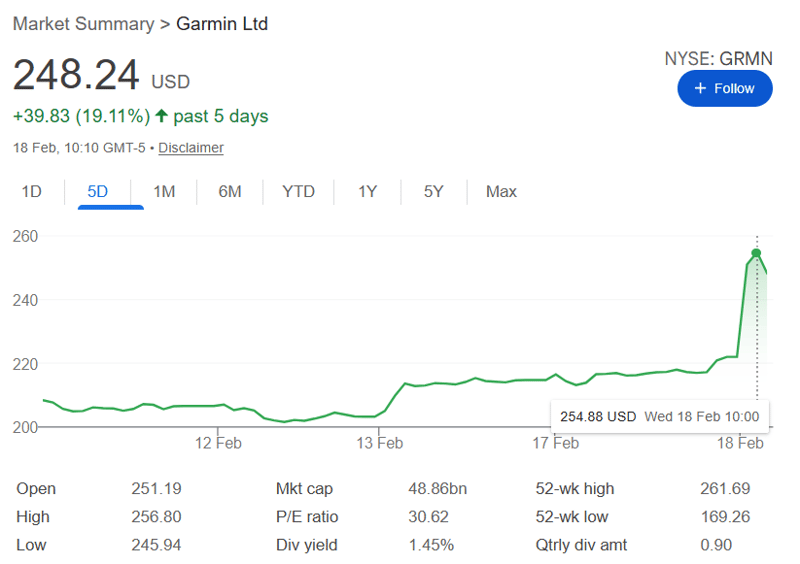

Garmin’s Q4 2025 results delivered earnings that literally moved the market. While the tech-heavy NASDAQ barely twitched, Garmin’s share price surged 20% on the news—a reaction driven almost entirely by one division: Fitness—the one that sells Forerunners and Edge bike computers. Here’s what happened and what it means.

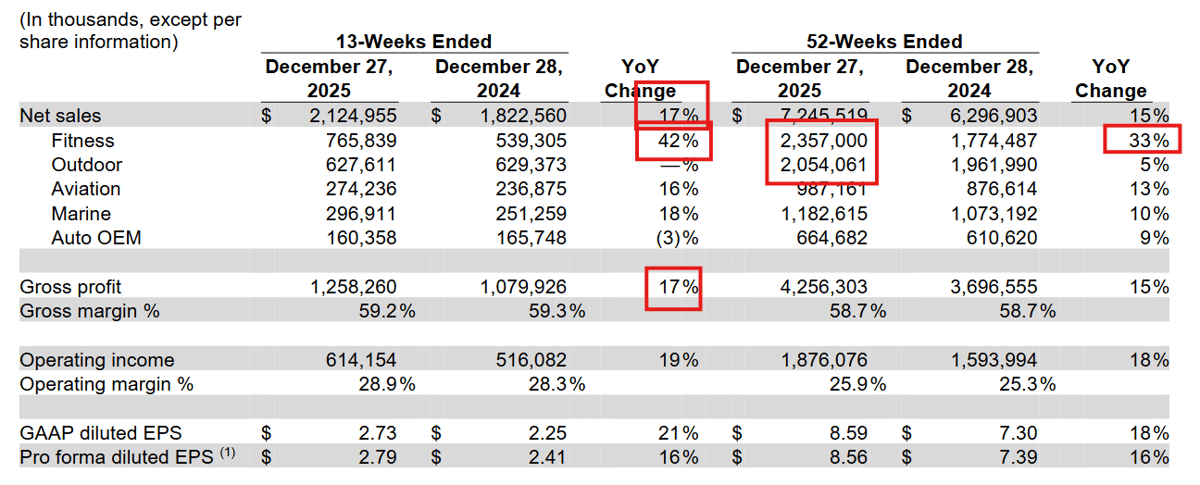

2025 was another year of remarkable growth and achievement for Garmin, with record consolidated revenue, record revenue in all five of our segments, and record consolidated operating income. [Pemble, CEO]

Fitness: Revenue increased 42% [in Q4]…driven by both market share gains and market growth…we announced our collaboration with Truemed to assist customers who wish to use pre-tax HSA/FSA funds for qualifying Garmin purchases…the Venu 4 and Forerunner 970 received [CES] Innovation Awards for novel features in digital health and fitness…enhancements to our premium Connect+ offering with nutrition tracking and insights powered by AI-based Garmin Active Intelligence.

Outdoor: Revenue from the outdoor segment was flat when compared to the prior year quarter, as we compare against strong prior year product launch cycles…Gross and operating margins were 66% and 37%…we launched the inReach Mini 3 Plus satellite communicator with voice, text and photo sharing…[the] Fenix 8 Pro-MicroLED [received a CES Innovation Award].

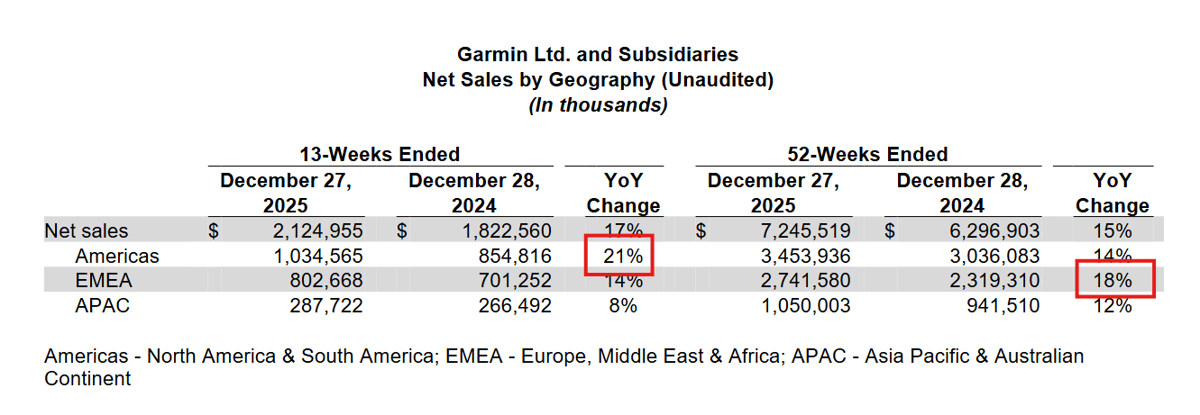

Geographically, Q4 was strong across all regions, with the Americas leading at 21% growth, EMEA at 14% and APAC at 8%. For the full year, EMEA was the standout region at 18% growth.

Garmin’s cash position continued to strengthen, ending Q4 with cash and marketable securities of over $4.1 billion — roughly double where it stood two years ago. Free cash flow for the full year was $1.36 billion.

Against Expectations

Good growth is one thing, but it only affects the share price if it differs from expectations. This quarter differed dramatically — in Garmin’s favour.

Analysts had expected Q4 pro forma EPS of around $2.39. Garmin delivered $2.79 — overperformance of nearly 17%. Revenue of $2.12 billion came in well ahead of the consensus of $2.01 billion. Combined with full-year 2026 guidance of $7.9 billion in revenue and pro forma EPS of $9.35, the market rewarded Garmin with a near-20% price gain while the NASDAQ barely moved. This is the mirror image of Q3, when Garmin fell 8% more than the market on outdoor underperformance.

My Personal Take: This share price move essentially corrects the shock of Fenix’s underperformance 3 months ago. Before that point GRMN had recently trended above the S&P500 after that point below it. Now it has returned above the S&P500 growth trajectory.

Fitness as Healthcare — The Truemed Story

The most strategically underappreciated announcement of the quarter was not a new watch — it was Garmin’s collaboration with Truemed, which allows US customers to use pre-tax Health Savings Account (HSA) and Flexible Spending Account (FSA) funds to purchase qualifying Garmin products. This is significant for several reasons.

HSA/FSA spending is tax-advantaged, meaning the effective price of a Garmin watch drops by 20–40% for eligible buyers, depending on their tax bracket. This removes a meaningful friction point for health-conscious consumers sitting on the fence. More importantly, it signals how Garmin is positioning itself as a health and wellness platform. That repositioning could have long-term valuation implications that extend well beyond this quarter’s results.

Outdoor: Flat is the New Problem

Outdoor revenue was flat in Q4 — technically an improvement on Q3’s 5% decline, but coming off already-reset expectations. For the full year, Outdoor grew just 5% against Fitness’s 33%. The Fenix 8 Pro and its MicroLED variant did not move the needle as the original Fenix 8 launch did in 2024. The comparable problem Garmin management flagged in Q3 has eased but has not been resolved. Outdoor remains Garmin’s second-largest segment by revenue at $2.05 billion for the full year, but the gap between it and Fitness ($2.36 billion) has now closed — and Fitness is accelerating, while Outdoor is treading water.

Key Takeaways for Garmin’s Future

If you are looking for hints and leaks on Garmin’s 2026 product range, try this detailed post. The likely thrust is towards range-gap filling and a new category competitor: CIRQA, a Whoop competitor.

- Fitness is now the company. At 42% Q4 growth and 33% for the year, the Fitness division — Forerunner, Edge, Venu — is no longer just Garmin’s largest segment. It is the segment that determines investor sentiment, drives the share price, and sets the tone for every earnings call. This is a structural shift, at least for now.

- Garmin is repositioning as health-tech. The Truemed HSA/FSA move, the King’s College London pregnancy study partnership, and the AI-powered Connect+ nutrition platform all point in the same direction: Garmin wants to be where fitness meets clinical health. That market is far larger — and more defensible — than sports wearables alone.

- Outdoor needs a catalyst. The Fenix 8 Pro and MicroLED didn’t provide the same lift as the original Fenix 8. With the comparable period now cycling through, 2026 is Outdoor’s opportunity to recover — but it needs a launch cycle that genuinely surprises, not one that consolidates.

- The share price reaction was rational. A 17% EPS beat, combined with record full-year results and solid 2026 guidance, warranted a repricing. The market had undervalued Garmin coming in — the 52-week low of $169 now appears to be a significant mispricing in hindsight.

- Outlook: 2026 guidance of $7.9 billion revenue (+9%) and $9.35 pro forma EPS is credible but not spectacular. The question heading into Q1 2026 is whether Fitness can sustain anything close to 30%+ growth rates, or whether a normalisation back toward 15–20% is already baked in. Management’s answer to that will matter more than any single product launch.

Sources & Resources

Garmin Q3 2025 Earnings: Fitness Explodes, Fenix 8 Pro Underwhelms

explosive Garmin Q2 Earnings – significant Forerunner 970 contribution (2025)

https://the5krunner.com/2025/04/30/strong-q1-earnings-from-garmin/

Last Updated on 19 March 2026 by the5krunner

Reader-Powered Content

This content is not sponsored. It’s mostly me behind the labour of love, which is this site, and I appreciate everyone who supports it.

Support the site: Follow (free, fewer ads) · Subscribe (paid, ad-free) · Buy Me A Coffee ❤️

All articles are written by real people, fact-checked, and verified for originality. See the Editorial Policy. FTC: Affiliate Disclosure — some links pay commission. As an Amazon Associate, I earn from qualifying purchases.

tfk is the founder and author of the5krunner, an independent endurance sports technology publication. With 20 years of hands-on testing of GPS watches and wearables, and competing in triathlons at an international age-group level, tfk provides in-depth expert analysis of fitness technology for serious athletes and endurance sport competitors.

Small correction: “Garmin’s cash position weakened slightly” is incorrect. The cash position actually stayed the same – and improved by $87m when taking into account marketable securities:

Cash and cash equivalents $ 2,072,208 $ 2,079,468

Marketable securities 515,038 421,270

The table/exhibit you posted is not cash position (which is a balance sheet item) but rather for (free) cash _flow_ during the period. And even then, the decline in free cash flow is quite benign because it is mostly due to a significant (> $200m) net increase in inventories – no doubt connected to the new device launches and in order to avoid OOS situations, like noted for the FR970.

If you go to Garmin Forums and compare the comment sections of the 570 and 970, it’s staggering….either the 570 is perfect out of the box with no bugs whatsoever…or no one is buying it….I suppose the latter.

But it seems the the Sleep Index Band has been delivered to the early adopters, because the first complain are coming in…Did you get one? I wonder how much the band data will deviate from the watch data.

in the context of this artcile i dont know how garmin books its revenue

it could invoice trade buyers of Index as it ships bulk volumes

i dont plan to get one. but i might eventally. if it was designed for sport i would