Global Smartwatch Market Returns to Growth in 2025, Driven by China and Premium Demand

Global smartwatch shipments grew 4% year on year in 2025, reversing a decline from the previous year, according to the latest full-year data from Counterpoint Research. This is a notable turnaround after five consecutive quarters of falling volumes through to early 2025.

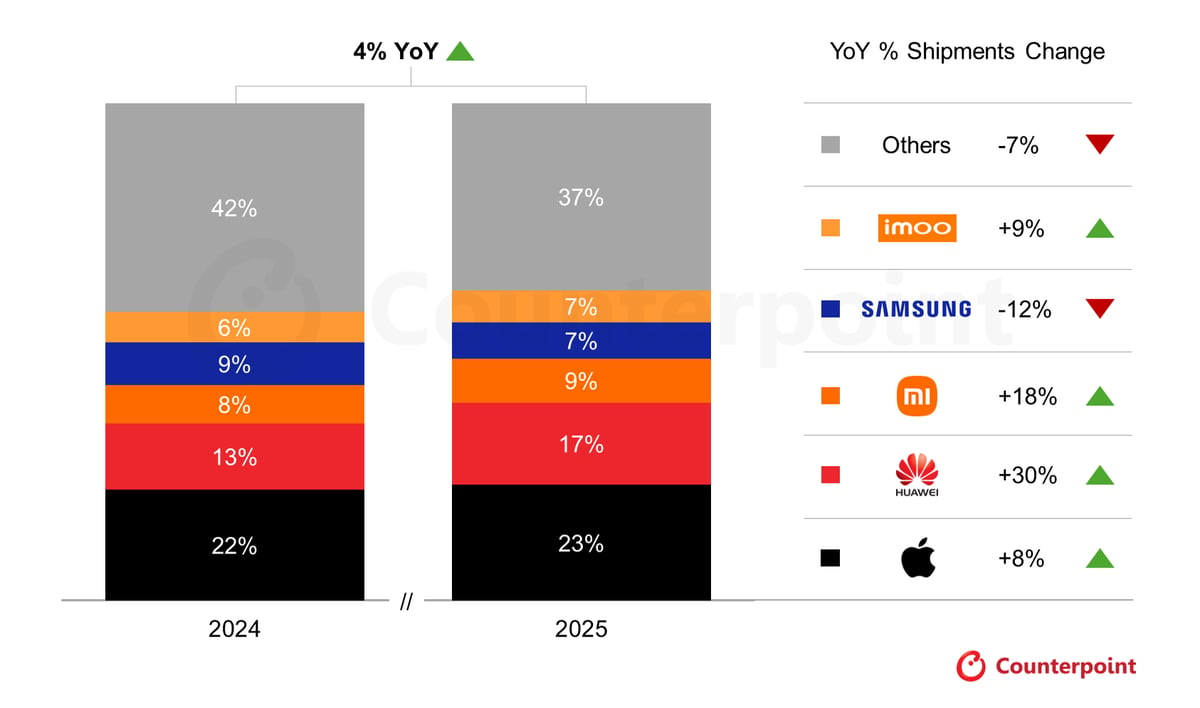

Domestic Chinese sales were the main engine. Large brands — led by Huawei, Xiaomi and children’s wearables maker Imoo — benefited from strong consumer demand, government subsidy programmes supporting electronics purchases, and deepening brand loyalty among Chinese buyers. China’s share of the global market is estimated to have risen from around 25% in 2024 to approximately 31% in 2025, the first year in which the country overtook North America to become the world’s largest market for advanced smartwatches.

Huawei recorded the highest growth in shipments among the top five brands globally, driven by competitively priced, advanced hardware and an expanding domestic ecosystem. The brand briefly surpassed Apple in global shipment rankings during the second quarter of 2025 — a first for the company.

Apple, however, staged a significant recovery of its own. The company posted its first year-on-year shipment growth since 2022, propelled by a refresh that introduced the Watch Series 11, Watch Ultra 3 and Watch SE 3. The updated range expanded Apple’s reach from the value-conscious buyer to the ultra-premium segment and incorporated meaningful advances, including 5G RedCap support, hypertension notifications, and satellite connectivity in the Ultra model. Analysts at Counterpoint noted that pent-up demand from buyers who had deferred purchases in anticipation of a substantially upgraded product played a material role in the revival.

The broader market’s recovery was not limited to volumes. Average selling prices rose 5% year-on-year, reflecting a structural shift toward premium devices. Shipments of smartwatches priced below $200 fell 9%, while the $200–$400 segment expanded by 48%. Even within entry-level tiers, average prices rose 34% as brands integrated artificial intelligence capabilities and advanced health sensors into lower-cost models.

Cellular-enabled smartwatches outpaced the overall market, with shipments rising 6% year on year. The category’s growth was driven by expanded health-monitoring features and emergency connectivity, which are increasingly positioning the smartwatch as a standalone device rather than a smartphone companion. Google, Garmin and Apple each introduced satellite connectivity during the year, reinforcing that trajectory.

India, by contrast, was a notable drag. The country’s once rapidly expanding market contracted sharply as demand for basic, low-cost smartwatches fell, unwinding growth that had made India one of the category’s most dynamic markets in prior years.

Counterpoint’s analysts project high-single-digit percentage growth for 2026, supported by continued premiumisation and the early commercial rollout of blood glucose (trend) monitoring technology, a capability that could broaden the health value proposition of the smartwatch materially.

Garmin, which competes primarily in the premium sports and outdoor segment, does not appear separately in Counterpoint’s top-five brand rankings. The company’s global shipment volumes are likely too small relative to the consumer mass-market leaders to register, the firm did introduce satellite connectivity features during 2025 and recorded growth in the third quarter.

Source: Counterpoint Research Global Smartwatch Shipments Tracker, Q4 2025, published February 2026.

Last Updated on 27 February 2026 by the5krunner

My favourite kit and nutrition

- Maurten — the race nutrition trusted by elite athletes. Gels and drink mix engineered to be easy on the stomach.

- Garmin 90-degree charging adapter — the small adapter that keeps your charging cable tidy at the stem. Essential for race day.

- Garmin charging puck — the fastest and most reliable way to top up your Garmin before a session.

- Ravemen FR300 — front light that mounts directly under your Garmin or Wahoo head unit. Keeps your bars clean and your beam pointed where it matters.

- Garmin Varia RTL515 — radar rear light that alerts you to vehicles approaching from behind. Pairs with your Edge or Garmin watch.

- Stryd — the footpod that brings running power to your Garmin. The single most useful running upgrade I have made.

- Favero Assioma Pro RS2 — the power meter pedals most serious cyclists end up choosing. Accurate, easy to move between bikes.

Reader-Powered Content

This content is not sponsored. It’s mostly me behind the labour of love, which is this site, and I appreciate everyone who supports it.

Support the site: Follow (free, fewer ads) · Subscribe (paid, ad-free) · Buy Me A Coffee ❤️

All articles are written by real people, fact-checked, and verified for originality. See the Editorial Policy. FTC: Affiliate Disclosure — some links pay commission. As an Amazon Associate, I earn from qualifying purchases.

tfk is the founder and author of the5krunner, an independent endurance sports technology publication. With 20 years of hands-on testing of GPS watches and wearables, and competing in triathlons at an international age-group level, tfk provides in-depth expert analysis of fitness technology for serious athletes and endurance sport competitors. ID