Garmin Is Growing From the Middle — Taking Share From Apple Above and Budget Brands Below

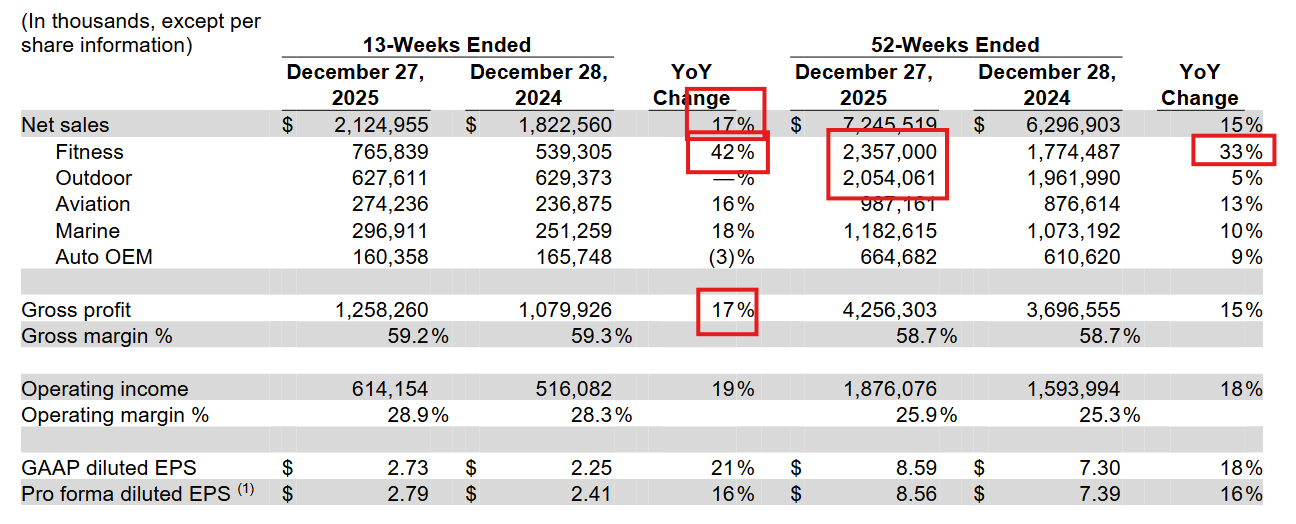

Garmin’s 33% year-over-year growth in fitness in 2025 demands an explanation. The wearables market is not currently growing at 33%. Companies that take share grow 33%. But which share, from whom, and is it sustainable? The Q4 2025 earnings call on 18 February 2026 gave the clearest answer Garmin has ever provided to these questions.

KeyBanc analyst Noah Zatzkin asked Pemble directly about the global wearables market and competitive dynamics. Pemble’s answer was unusually specific:

The overall market has been on a growth path — I would call it steady growth, mid-singles up to 10% kind of range. That’s one driver of our overall growth. But market share has been a really important one for us as well, as we’ve been able to take share both above and below us from different players. People recognise the value of our products and the uniqueness of the features that they offer.

“Above and below” is the operative phrase. Above Garmin sits Apple, whose Apple Watch dominates the mainstream smartwatch market in terms of volume. Below sits a proliferation of Chinese manufacturers — Xiaomi, Amazfit, Huawei and others — offering fitness tracking at price points that undercut traditional sports watch brands. Garmin is growing by winning customers from both ends of that spectrum simultaneously.

From Apple, Garmin is pulling buyers who want genuine sports performance depth — particularly the training ecosystem: structured workout planning, recovery metrics, race predictor, and the kind of long-term training load analysis that Apple Watch struggles or fails to offer at any price point. The Forerunner 970 and Venu 4 are the clearest examples: premium smartwatch aesthetics combined with sports science depth that Apple has not matched.

From the Chinese brands, Garmin is winning on ecosystem quality and data trustworthiness. A Xiaomi band may track steps adequately. It cannot offer the depth of Garmin Coach, the accuracy of Garmin’s GPS platforms, or the credibility of its ecosystem. As health-conscious consumers become more sophisticated, the quality gap matters more.

Pemble had previously referenced this dynamic in Q3 2025, where he said, “we are a small but growing market share player in the overall wearables market.” That framing is instructive. Even after 33% growth, Garmin’s absolute market share in the broader smartwatch category remains modest. The runway is long.

The market growth number — mid-singles to 10% — provides the baseline. If the overall market is growing at 8% and Garmin is growing at 33%, then approximately 25 percentage points of that growth is pure share gain. At $2.36 billion in annual fitness revenue, that is a significant and accelerating competitive advantage.

For consumers, this competitive dynamic is a gift. Garmin is motivated to keep innovating rapidly, keep pricing competitive (also noted was that Garmin is achieving growth not by raising prices as widely believed), and keep the feature gap wide — because the moment it stops doing those things, Apple has the brand muscle and distribution to take back those converts. The running and cycling community is currently benefiting from a company fighting hard to maintain its position. Long may it continue.

Commentary

This data confounds some of my long-held expectations. For several years, I have believed and repeatedly stated that the endgame would see Garmin squeezed from both ends — Apple becoming sufficiently capable at high-end sports to erode the case for uber-premium devices (Fenix 8 microLED, Fenix 9), while lower-end brands grew increasingly competent and undercut on price for the same features. That structural pressure is real and still playing out.

But it hasn’t translated into market share loss — yet. Apple still cannot match Garmin’s sports training ecosystem, and lower-end brands tend to offer capable hardware with ecosystems that are currently too underdeveloped to credibly compete. Garmin is holding the middle ground better than I expected.

Sport is not the whole story, though. Smart features and full-day wearability matter too, and Garmin has historically been weaker there. It is making headway, and EU regulatory pressure forcing Apple to open up some ringfenced features is quietly helping Garmin’s competitive position.

Two other factors may be doing more work than any of the above. Battery life remains a genuine differentiator — and as long as it does, budget brands will struggle to meet the needs of many athletes. And there may be a demographic and sentiment dimension: buyers who want to associate their watch with a sporting identity and choose Garmin for what it says about them, not just what it does. That is a harder position for any competitor to erode.

I’ll stick with my predictions of a Big Squeeze for Garmin. It’s just that it’s not happening any time soon!

Last Updated on 16 March 2026 by the5krunner

Reader-Powered Content

This content is not sponsored. It’s mostly me behind the labour of love, which is this site, and I appreciate everyone who supports it.

Support the site: Follow (free, fewer ads) · Subscribe (paid, ad-free) · Buy Me A Coffee ❤️

All articles are written by real people, fact-checked, and verified for originality. See the Editorial Policy. FTC: Affiliate Disclosure — some links pay commission. As an Amazon Associate, I earn from qualifying purchases.

tfk is the founder and author of the5krunner, an independent endurance sports technology publication. With 20 years of hands-on testing of GPS watches and wearables, and competing in triathlons at an international age-group level, tfk provides in-depth expert analysis of fitness technology for serious athletes and endurance sport competitors.