The Loyalty Gap: Garmin and Coros Owners Most Likely to Switch

A new consumer survey puts a number on something the sports watch industry has probably suspected for a while. Nearly 56% of smartwatch owners say they are open to switching brands. Among Apple Watch owners, that figure drops to 38%. Garmin and Coros owners sit well above that – more willing to switch than any other major sports watch brand.

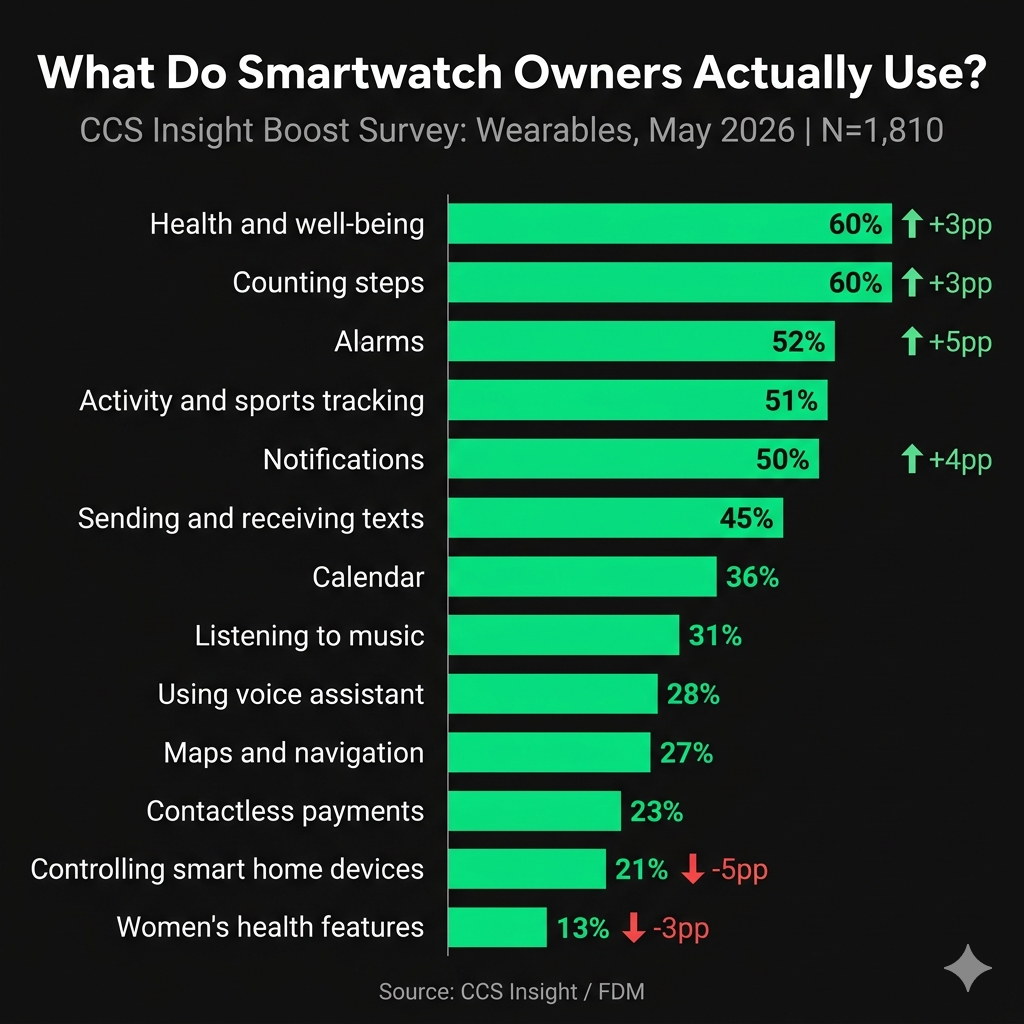

The data comes from CCS Insight’s Boost Survey: Wearables, published May 2026, covering 1,810 smartwatch owners and users across Germany, Spain, the UK, the US and India.

The loyalty gap has a straightforward explanation. Apple Watch owners are buying into a phone ecosystem, a health platform, an app library, and a payments system. Switching watch brands means friction across all of those. The cost of leaving is high.

Garmin and Coros owners face no equivalent switching cost. Their watches talk to third-party platforms. Strava, TrainingPeaks, and Komoot do not care which watch you wear. A Garmin user eyeing a Coros Pace 4, an Apple Watch Ultra, or a Polar Vantage 3 faces an ever-smaller ecosystem penalty for moving. The watch is the product. Nothing else locks them into the downstream analytic and social tools.

That is a structural problem for the sports watch brands. They compete on hardware and software features in a market where customers have every reason to shop around. Every product cycle is a retention event. Miss on battery life, GPS accuracy, training load metrics, or price, and the door is open.

Apple only needs to be good enough in sports. The Ultra has closed most of the functional gap with dedicated sports watches for most endurance athletes who are not at the sharp end of performance. For that user, the switching cost calculation runs firmly in Apple’s favour.

This site has argued at length that the structural cracks in Garmin’s empire are already visible. The CCS Insight loyalty data adds consumer evidence to that argument. It is one thing to identify strategic vulnerabilities at the business level. It is another to see them reflected in the willingness of actual customers to walk or, at least, to talk about walking.

The survey findings also have implications for how sports brands should think about new features. Ecosystem depth — connecting the watch more tightly to proprietary coaching platforms, health services, or third-party integrations — is one of the few levers available. Garmin Connect, Garmin Coach, and the Connect IQ platform are moves in that direction. So is Coros’s decision to open its data to AI platforms via MCP — a bet that deeper data access creates stickiness. Neither brand has yet to create the kind of lock-in that keeps a customer as well as Apple.

The 56% overall switching intention figure is also a market opportunity. More than half of smartwatch owners are, in principle, available. The brands that articulate a clear reason to switch, and remove the friction of doing so, stand to gain.

For Garmin and Coros, the loyalty data is a warning. For Apple, it is confirmation that the ecosystem strategy is working exactly as intended.

What the Data Shows

- 56% of smartwatch owners overall are open to switching brands

- Apple Watch owners: only 38% open to switching — the most loyal segment

- Fitbit users: over 70% open to switching — the least loyal segment

- Survey base: 1,810 smartwatch owners and users across Germany, Spain, the UK, the US and India

- Source: CCS Insight Boost Survey: Wearables, May 2026

Why Ecosystem Lock-In Is Key To Long-Term Survival

The gap between 38% and 56% is significant. It reflects a fundamental structural advantage that Apple has built over a decade of ecosystem investment. When a customer buys an Apple Watch, they are also deepening their dependency on iPhone, iCloud, Apple Health, Apple Pay, and AirPods. Each of those integrations raises the cost of switching to a competing platform.

Sports watch brands have not built an equivalent. Garmin’s move into the recovery-wearable space with CIRQA is one attempt to extend the ecosystem beyond the watch. But a recovery band alone does not replicate the depth of Apple’s integration across productivity, communication, and payments.

The comparison with what Garmin continues to do wrong strategically is instructive. The loyalty data is consumer-level evidence that a strategy has not yet solved the retention problem.

Data source: CCS Insight Boost Survey: Wearables, May 2026. Base: 1,810 smartwatch owners and users in Germany, Spain, the UK, the US and India.

Last Updated on 3 June 2026 by the5krunner

My favourite kit and nutrition

- Maurten — the race nutrition trusted by elite athletes. Gels and drink mix engineered to be easy on the stomach.

- Garmin 90-degree charging adapter — the small adapter that keeps your charging cable tidy at the stem. Essential for race day.

- Garmin charging puck — the fastest and most reliable way to top up your Garmin before a session.

- Ravemen FR300 — front light that mounts directly under your Garmin or Wahoo head unit. Keeps your bars clean and your beam pointed where it matters.

- Garmin Varia RTL515 — radar rear light that alerts you to vehicles approaching from behind. Pairs with your Edge or Garmin watch.

- Stryd — the footpod that brings running power to your Garmin. The single most useful running upgrade I have made.

- Favero Assioma Pro RS2 — the power meter pedals most serious cyclists end up choosing. Accurate, easy to move between bikes.

Reader-Powered Content

This content is not sponsored. It’s mostly me behind the labour of love, which is this site, and I appreciate everyone who supports it.

Support the site: Follow (free, fewer ads) · Subscribe (paid, ad-free) · Buy Me A Coffee ❤️

All articles are written by real people, fact-checked, and verified for originality. See the Editorial Policy. FTC: Affiliate Disclosure — some links pay commission. As an Amazon Associate, I earn from qualifying purchases.

tfk is the founder and author of the5krunner, an independent endurance sports technology publication. With 20 years of hands-on testing of GPS watches and wearables, and competing in triathlons at an international age-group level, tfk provides in-depth expert analysis of fitness technology for serious athletes and endurance sport competitors. ID

Ecosystem lock‑in is a deal-breaker for me. I prefer the freedom to switch brands and devices based on my needs, budget, and priorities. Buying a device already requires compromises — features, price, battery life, usability — so adding artificial restrictions on top of that doesn’t make sense.

While ecosystems can offer benefits, they also create a sense of being trapped because you’ve invested too much to leave. I’d rather keep my options open than feel locked into a system that no longer fits my needs.

As an old (in two senses 🙂 Garmin user I do have some lock with Garmin. Many ANT+ only sensors and a belief that even my dual sensors like Stryd are better to be used with ANT+ and not BT.

So I was trapped via ANT+ by Garmin.

Just an example: what the hell I should do with my 5 Tempe sensors? 🙂